##########################################################################################

##########################################################################################

### ###

### ############################# ######### ######### ###

### ################################# ######### ######### ###

### #################################### ######### ######### ###

### ######## ######### ######### ######### ###

### ######## C3_BIG_SPARK_MAX ######### ######### ######### ###

### ######## +TSV9 ######### ######### ######### ###

### ######## @Christopher84 ######### ######### ######### ###

### ######## ######### ######### ######### ###

### ###################################### ################################## ###

### #################################### ################################## ###

### ################################# ################################## ###

### #################################### ################################## ###

### ######## ######### ######### ###

### ######## @Horserider ######### ######### ###

### ######## HORSERIDER VOLUME ######### ######### ###

### ######## TRIPLE EXHAUSTION ######### ######### ###

### ######## @chence27 ######### ######### ###

### ######## ######### ######### ###

### #################################### ######### ###

### ################################## ######### ###

### ############################### ######### ###

### ###

##########################################################################################

##########################################################################################

input use_EMAD_filter = yes;

input Arrow_filter = 2; #hint number of conditions met must be greater than

input Show_filter_Cloud = no;

input Cloud_filter = 0; #hint number of conditions met must be greater than

input controlpercent = 50;

input show_TS_lastlabel = yes; #hint shows which TS_V9 signal is most recent

input show_filter_TS = yes;

input show_TS_V9_Lines = no; #Show horizontal long and short entry exit lines

input Use_Arrow_Inputs = yes;

input Use_Alert4_UP_C = yes;

input Use_Alert4_DN_C = yes;

input Use_signal_UP_C = yes; #hint Big4 signal up signal as part of "Allup" signal count

input Use_signal_DN_C = yes; #hint Big4 signal down as part of "Alldown" signal count

input Use_signal_2_UP_C = yes; #hint Big4 signal up signal as part of "Allup" signal count

input Use_signal_2_DN_C = yes; #hint Big4 signal down as part of "Alldown" signal count

input Use_Spark_UP_C = yes;

input Use_Spark_DN_C = yes;

input Use_Spark_DN2_C = yes;

input Use_Spark_UP2_C = no;

input Use_TS_UP_C = yes; #hint TS_V9 up signal as part of "Allup" signal count

input Use_TS_DN_C = yes; #hint TS_V9 down signal as part of "Alldown" signal count

input Use_TripleEx_UP_C = yes; #hint triple exhaustion

input Use_TripleEx_DN_C = yes; #hint triple exhaustion

input ShowEMAcloud = no; #hint default C3_Max cloud Average 8 and 9

input showall = no; #hint show all signals individually

input length_HV = 20; #Horserider Volume Average

input showLabels = yes; #hint C3_Max

input tradeDaytimeOnly = no; #hint tradeDaytimeOnly: (IntraDay Only) Only perform trades during hours stated

input OpenTime = 0930; #hint OpenTime: Opening time of market

input CloseTime = 1600; #hint CloseTime: Closing time of market

input VolumeTime = 1030; #hint OpenTime: Opening time of market

input Strategy_Confirmation_Factor = 4; #hint Big4

input TargetMultiple = 0.5; #hint TS_V9

input control = 13; #hint percent distance from current price to key level (0 is at level)

input showbubbles = no; #hint TS_V9

input type = { default SMP, EXP }; #hint TS_V9

input trailType = {default modified, unmodified}; #hint TS_V9

input averagetype = AverageType.SIMPLE;

input MACD_AverageType = {SMA, default EMA};

input DMI_averageType = AverageType.WILDERS;

input AvgType = AverageType.HULL;

input firstTrade = {default long, short}; #hint TS_V9

input ehlers_length = 13;

def hotpct = 150; #hint Horserider High Volume indication

def elhers3length = 9;

def Triple_Ex_Lookback = 15;

def Triple_Ex_Control = 2;

def lookbackcontrol = 1;

def lookbackcontrol2 = 1;

def arrowfilter = 12;

def keyleveltolerance = 1;

def showverticallineday = yes;

def show_ts_signals = no;

def length9 = 35;

def length8 = 10;

def length10 = 20;

def length_3x = 1000;

def LongTrades = yes; #hint LongTrades: perform long tradesvb balanceOfMarketPower AbandonedBaby b bbbbbbbbg

def ShortTrades = yes; #hint ShortTrades: perform short trades

def useStops = no; #hint useStops: use stop orders

def useAlerts = no; #hint useAlerts: use alerts on signals

def ATRPeriod = 11;

def ATRFactor = 2.2;

def ATRPeriod2 = 5;

def ATRFactor2 = 1.5;

def AtrMult = 1.0;

def HideBoxLines = no;

def HideCloud = no;

def HideLabels = no;

def Strategy_FilterWithTMO = no;

def Strategy_FilterWithTMO_arrows = yes;

def Strategy_HoldTrend = no;

def Strategy_ColoredCandlesOn = yes;

def coloredCandlesOn = yes;

def ColorPrice = yes;

def color_blst = no;

def color_3x = yes;

def color_3xt = yes;

def color_OBOS = no;

def BarsUsedForRange = 2;

def BarsRequiredToRemainInRange = 2;

def trig = 20;# for Blast-off candle color

def HideTargets = no;

def HideBalance = no;

#USER INPUTS

## Upper and Lower EMAD Lines

def fastLength_EMAD = 10;

def slowLength_EMAD = 35;

def smoothLength_EMAD = 12;

def smoothLength2_EMAD = 14;

def priceType_EMAD = close;

def emadLineWeight_EMAD = 2;

def showEMACloud_EMAD = yes;

def showBubbles_EMAD = yes;

def averageType_EMAD = AverageType.WILDERS;

## Upper and Lower Band Lines

def bandLength_EMAD = 100;

def bandLength2_EMAD = 200;

#DEFINITIONS / CALCULATIONS

## UPPER EMAD LINE

def fastExpAvg_EMAD = ExpAverage(priceType_EMAD, fastLength_EMAD);

def slowExpAvg_EMAD = ExpAverage(priceType_EMAD, slowLength_EMAD);

def EMAD_EMAD = (priceType_EMAD - fastExpAvg_EMAD);

def EMAD2_EMAD = (priceType_EMAD - slowExpAvg_EMAD);

def EMADAvg_EMAD = (EMAD_EMAD + EMAD2_EMAD) / 2;

def upperEMADLine_EMAD = ExpAverage(EMADAvg_EMAD, smoothLength_EMAD);

## LOWER EMAD LINE

def emadOpen_EMAD = (upperEMADLine_EMAD + upperEMADLine_EMAD[1]) / 2;

def emadHigh_EMAD = Max(upperEMADLine_EMAD, upperEMADLine_EMAD[1]);

def emadLow_EMAD = Min(upperEMADLine_EMAD, upperEMADLine_EMAD[1]);

def emadClose_EMAD = upperEMADLine_EMAD;

def bottom_EMAD = Min(emadClose_EMAD[1], emadLow_EMAD);

def tr_EMAD = TrueRange(emadHigh_EMAD, emadClose_EMAD, emadLow_EMAD);

def ptr_EMAD = tr_EMAD / (bottom_EMAD + tr_EMAD / 2);

def APTR_EMAD = MovingAverage(averageType_EMAD, ptr_EMAD, smoothLength2_EMAD);

def upperBand_EMAD = emadClose_EMAD[1] + (APTR_EMAD * emadOpen_EMAD);

def lowerBand_EMAD = emadClose_EMAD[1] - (APTR_EMAD * emadOpen_EMAD);

def lowerEMADLine_EMAD = (upperBand_EMAD + lowerBand_EMAD) / 2;

## TOP AND BOTTOM BANDS

def zeroLineData_EMAD = if IsNaN(close) then Double.NaN else 0;

def EMADSUp_EMAD = upperEMADLine_EMAD > zeroLineData_EMAD;

def EMADSDown_EMAD = upperEMADLine_EMAD < zeroLineData_EMAD;

def EMADdown_EMAD = (lowerEMADLine_EMAD > upperEMADLine_EMAD);

def EMADup_EMAD = (upperEMADLine_EMAD >= lowerEMADLine_EMAD);

def topBand_EMAD = Highest(lowerEMADLine_EMAD, bandLength_EMAD);

def bottomBand_EMAD = Lowest(lowerEMADLine_EMAD, bandLength_EMAD);

## BAND DIRECTION (USED ONLY FOR COLORING - NOT USED FOR PLOTS)

def topBandStepDown_EMAD = if topBand_EMAD < topBand_EMAD[1] then 1 else 0;

def topBandStepUp_EMAD = if topBand_EMAD > topBand_EMAD[1] then 1 else 0;

def bottomBandStepDown_EMAD = if bottomBand_EMAD < bottomBand_EMAD[1] then 1 else 0;

def bottomBandStepUp_EMAD = if bottomBand_EMAD > bottomBand_EMAD[1] then 1 else 0;

def bothBandsDown_EMAD = bottomBandStepDown_EMAD and topBandStepDown_EMAD;

def bothBandsUp_EMAD = bottomBandStepUp_EMAD and topBandStepUp_EMAD;

def bullBias_EMAD = (bottomBand_EMAD > zeroLineData_EMAD);

def bearBias_EMAD = (topBand_EMAD < zeroLineData_EMAD);

## BUBBLE CALCULATIONS (USED ONLY FOR BUBBLES)

def midBand_EMAD = (upperBand_EMAD + lowerBand_EMAD) / 2;

def crossesUp_EMAD = if (midBand_EMAD[1] > upperEMADLine_EMAD[1]) and (midBand_EMAD < upperEMADLine_EMAD) then 1 else 0;

def crossesDown_EMAD = if (upperEMADLine_EMAD[1] > midBand_EMAD[1]) and (upperEMADLine_EMAD < midBand_EMAD) then 1 else 0;

def valueUp_EMAD = if crossesUp_EMAD then midBand_EMAD else 0;

def valueDown_EMAD = if crossesDown_EMAD then midBand_EMAD else 0;

def crossesUpline_EMAD = if (valueUp_EMAD - bottomBand_EMAD) == 0 then 1 else 0;

def crossesDownline_EMAD = if (valueDown_EMAD - topBand_EMAD) == 0 then 1 else 0;

def crossesUpline_filter_EMAD = if crossesUpline_EMAD and (crossesUpline_EMAD[1] or crossesUpline_EMAD[2] or crossesUpline_EMAD[3] or crossesUpline_EMAD[4]) then 0 else 1;

def crossesDownline_filter_EMAD = if crossesDownline_EMAD and (crossesDownline_EMAD[1] or crossesDownline_EMAD[2] or crossesDownline_EMAD[3] or crossesDownline_EMAD[4]) then 0 else 1;

#PLOTS

def zeroLine_EMAD = zeroLineData_EMAD;

def upperEMADLinePlot_EMAD = upperEMADLine_EMAD;

def lowerEMADLinePlot_EMAD = lowerEMADLine_EMAD;

def masterEMADLinePlot_EMAD = (upperEMADLinePlot_EMAD + lowerEMADLinePlot_EMAD) / 2;

def topBandPlot_EMAD = topBand_EMAD;

def bottomBandPlot_EMAD = bottomBand_EMAD;

def topunderzero = topBandPlot_EMAD < zeroLine_EMAD;

def bottomunderzero = bottomBandPlot_EMAD > zeroLine_EMAD;

def emaunderzero = upperEMADLinePlot_EMAD < zeroLine_EMAD;

def emaabovezero = upperEMADLinePlot_EMAD > zeroLine_EMAD;

def EMADaboveZero = emaabovezero or emaabovezero[1];

def EMADbelowZero = emaunderzero or emaunderzero[1];

def toppushline = masterEMADLinePlot_EMAD >= topbandPlot_EMAD;

def bottompushline = masterEMADLinePlot_EMAD <= bottomBandPlot_EMAD;

#####################################################

#TS Strategy_V9 Created by Christopher84 08/10/2021

#####################################################

Assert(ATRFactor > 0, "'atr factor' must be positive: " + ATRFactor);

def HiLo = Min(high - low, 1.5 * Average(high - low, ATRPeriod));

def HRef = if low <= high[1]

then high - close[1]

else (high - close[1]) - 0.5 * (low - high[1]);

def LRef = if high >= low[1]

then close[1] - low

else (close[1] - low) - 0.5 * (low[1] - high);

def trueRange;

switch (trailType) {

case modified:

trueRange = Max(HiLo, Max(HRef, LRef));

case unmodified:

trueRange = TrueRange(high, close, low);

}

def loss = ATRFactor * MovingAverage(averageType, trueRange, ATRPeriod);

def state = {default init, long, short};

def trail;

switch (state[1]) {

case init:

if (!IsNaN(loss)) {

switch (firstTrade) {

case long:

state = state.long;

trail = close - loss;

case short:

state = state.short;

trail = close + loss;

}

} else {

state = state.init;

trail = Double.NaN;

}

case long:

if (close > trail[1]) {

state = state.long;

trail = Max(trail[1], close - loss);

} else {

state = state.short;

trail = close + loss;

}

case short:

if (close < trail[1]) {

state = state.short;

trail = Min(trail[1], close + loss);

} else {

state = state.long;

trail = close - loss;

}

}

def price = close;

def TrailingStop = trail;

def LongEnter = (price crosses above TrailingStop);

def LongExit = (price crosses below TrailingStop);

def upsignal = (price crosses above TrailingStop);

def downsignal = (price crosses below TrailingStop);

def Begin = SecondsFromTime(OpenTime);

def End = SecondsTillTime(CloseTime);

def isIntraDay = if GetAggregationPeriod() > 14400000 or GetAggregationPeriod() == 0 then 0 else 1;

def MarketOpen = if !tradeDaytimeOnly or !isIntraDay then 1 else if tradeDaytimeOnly and isIntraDay and Begin > 0 and End > 0 then 1 else 0;

def PLBuySignal3 = if MarketOpen and (upsignal) then 1 else 0 ; # insert condition to create long position in place of the 0>0

def PLSellSignal3 = if MarketOpen and (downsignal) then 1 else 0; # insert condition to create short position in place of the 0>0

def PLBuyStop = if !useStops then 0 else if (0 > 0) then 1 else 0 ; # insert condition to stop in place of the 0<0

def PLSellStop = if !useStops then 0 else if (0 > 0) then 1 else 0 ; # insert condition to stop in place of the 0>0

def PLMktStop = if MarketOpen[-1] == 0 then 1 else 0; # If tradeDaytimeOnly is set, then stop at end of day

def PLBuySignal = if MarketOpen and (upsignal) then 1 else 0 ; # insert condition to create long position in place of the 0>0

def PLSellSignal = if MarketOpen and (downsignal) then 1 else 0; # insert condition to create short position in place 0>0

def CurrentPosition; # holds whether flat = 0 long = 1 short = -1

if (BarNumber() == 1) or IsNaN(CurrentPosition[1]) {

CurrentPosition = 0;

} else {

if CurrentPosition[1] == 0 { # FLAT

if (PLBuySignal and LongTrades) {

CurrentPosition = 1;

} else if (PLSellSignal and ShortTrades) {

CurrentPosition = -1;

} else {

CurrentPosition = CurrentPosition[1];

}

} else if CurrentPosition[1] == 1 { # LONG

if (PLSellSignal and ShortTrades) {

CurrentPosition = -1;

} else if ((PLBuyStop and useStops) or PLMktStop or (PLSellSignal and ShortTrades == 0)) {

CurrentPosition = 0;

} else {

CurrentPosition = CurrentPosition[1];

}

} else if CurrentPosition[1] == -1 { # SHORT

if (PLBuySignal and LongTrades) {

CurrentPosition = 1;

} else if ((PLSellStop and useStops) or PLMktStop or (PLBuySignal and LongTrades == 0)) {

CurrentPosition = 0;

} else {

CurrentPosition = CurrentPosition[1];

}

} else {

CurrentPosition = CurrentPosition[1];

}

}

def isLong = if CurrentPosition == 1 then 1 else 0;

def isShort = if CurrentPosition == -1 then 1 else 0;

def isFlat = if CurrentPosition == 0 then 1 else 0;

#Addorder(OrderType.BUY_AUTO, condition = LongEnter, price = open[-1], 1, tickcolor = GetColor(1), arrowcolor = Color.LIME);

#AddOrder(OrderType.SELL_AUTO, condition = LongExit, price = open[-1], 1, tickcolor = GetColor(2), arrowcolor = Color.LIME);

def BuySig = if (((isShort[1] and LongTrades) or (isFlat[1] and LongTrades)) and PLBuySignal) then 1 else 0;

def SellSig = if (((isLong[1] and ShortTrades) or (isFlat[1] and ShortTrades)) and PLSellSignal) then 1 else 0;

def bn = barnumber();

def TS_UP1bn = if upsignal[1] then BN else TS_UP1bn[1];

def TS_DN1bn = if downsignal[1] then BN else TS_DN1bn[1];

def cond13_TS_Buy = Buysig;

def cond13_TS_Sell = Sellsig;

def TS_Last = if TS_UP1bn > TS_DN1bn then 1 else 0;

###############################################

##OB_OS_Levels_v5 by Christopher84 12/10/2021

###############################################

#def TrailingStop = trail;

def H = Highest(TrailingStop, 12);

def L = Lowest(TrailingStop, 12);

def BulgeLengthPrice = 100;

def SqueezeLengthPrice = 100;

def BandwidthC3 = (H - L);

#def IntermResistance2 = Highest(BandwidthC3, BulgeLengthPrice);

def IntermSupport2 = Lowest(BandwidthC3, SqueezeLengthPrice);

def sqzTrigger = BandwidthC3 <= IntermSupport2;

def sqzLevel = if !sqzTrigger[1] and sqzTrigger then hl2

else if !sqzTrigger then Double.NaN

else sqzLevel[1];

###############################################

##Yellow Candle_height (OB_OS)

###############################################

def displace = 0;

def factorK2 = 3.25;

def lengthK2 = 20;

def price1 = open;

def trueRangeAverageType = AverageType.SIMPLE;

def ATR_length = 15;

def SMA_lengthS = 6;

def HiLo2 = Min(high - low, 1.5 * Average(high - low, ATRPeriod));

def HRef2 = if low <= high[1]

then high - close[1]

else (high - close[1]) - 0.5 * (low - high[1]);

def LRef2 = if high >= low[1]

then close[1] - low

else (close[1] - low) - 0.5 * (low[1] - high);

def loss2 = ATRFactor2 * MovingAverage(averageType, trueRange, ATRPeriod2);

def multiplier_factor = 1.25;

def valS = Average(price, SMA_lengthS);

def average_true_range = Average(TrueRange(high, close, low), length = ATR_length);

def Upper_BandS = valS[-displace] + multiplier_factor * average_true_range[-displace];

def Middle_BandS = valS[-displace];

def Lower_BandS = valS[-displace] - multiplier_factor * average_true_range[-displace];

def shiftK2 = factorK2 * MovingAverage(trueRangeAverageType, TrueRange(high, close, low), lengthK2);

def averageK2 = MovingAverage(averageType, price, lengthK2);

def AvgK2 = averageK2[-displace];

def Upper_BandK2 = averageK2[-displace] + shiftK2[-displace];

def Lower_BandK2 = averageK2[-displace] - shiftK2[-displace];

def condition_BandRevDn = (Upper_BandS > Upper_BandK2);

def condition_BandRevUp = (Lower_BandS < Lower_BandK2);

def fastLength = 12;

def slowLength = 26;

def MACDLength = 9;

def fastEMA = ExpAverage(price, fastLength);

def slowEMA = ExpAverage(price, slowLength);

def Value;

def Avg;

switch (MACD_AverageType) {

case SMA:

Value = Average(price, fastLength) - Average(price, slowLength);

Avg = Average(Value, MACDLength);

case EMA:

Value = fastEMA - slowEMA;

Avg = ExpAverage(Value, MACDLength);

}

def Diff = Value - Avg;

def MACDLevel = 0.0;

def Level = MACDLevel;

def condition1_Yellow_Candle = Value[1] <= Value;

def condition1D_Yellow_Candle = Value[1] > Value;

##########

#RSI

##########

def RSI_length = 14;

def RSI_AverageType = AverageType.WILDERS;

def RSI_OB = 70;

def RSI_OS = 30;

def NetChgAvg = MovingAverage(RSI_AverageType, price - price[1], RSI_length);

def TotChgAvg = MovingAverage(RSI_AverageType, AbsValue(price - price[1]), RSI_length);

def ChgRatio = if TotChgAvg != 0 then NetChgAvg / TotChgAvg else 0;

def RSI = 50 * (ChgRatio + 1);

def condition2_RSI = (RSI[3] < RSI) is true or (RSI >= 80) is true;

def condition2D_RSI = (RSI[3] > RSI) is true or (RSI < 20) is true;

def conditionOB1_RSI = RSI > RSI_OB;

def conditionOS1_RSI = RSI < RSI_OS;

########

#MFI

########

def MFI_Length = 14;

def MFIover_Sold = 20;

def MFIover_Bought = 80;

def movingAvgLength = 1;

def MoneyFlowIndex = Average(MoneyFlow(high, close, low, volume, MFI_Length), movingAvgLength);

def MFIOverBought = MFIover_Bought;

def MFIOverSold = MFIover_Sold;

def condition3_MFI = (MoneyFlowIndex[2] < MoneyFlowIndex) is true or (MoneyFlowIndex > 85) is true;

def condition3D_MFI = (MoneyFlowIndex[2] > MoneyFlowIndex) is true or (MoneyFlowIndex < 20) is true;

def conditionOB2_MFI = MoneyFlowIndex > MFIover_Bought;

def conditionOS2_MFI = MoneyFlowIndex < MFIover_Sold;

#############

#Forecast

#############

def na = Double.NaN;

def MidLine = 50;

def Momentum = MarketForecast().Momentum;

def NearT = MarketForecast().NearTerm;

def Intermed = MarketForecast().Intermediate;

def FOB = 80;

def FOS = 20;

def upperLine = 110;

def condition4_Forcast = (Intermed[1] <= Intermed) or (NearT >= MidLine);

def condition4D_Forcast = (Intermed[1] > Intermed) or (NearT < MidLine);

def conditionOB3_Forcast = Intermed > FOB;

def conditionOS3_Forcast = Intermed < FOS;

def conditionOB4_Forcast = NearT > FOB;

def conditionOS4_Forcast = NearT < FOS;

####################

#Change in Price

####################

def lengthCIP = 5;

def CIP = (price - price[1]);

def AvgCIP = ExpAverage(CIP[-displace], lengthCIP);

def CIP_UP = AvgCIP > AvgCIP[1];

def CIP_DOWN = AvgCIP < AvgCIP[1];

def condition5_CIP = CIP_UP;

def condition5D_CIP = CIP_DOWN;

###########

#EMA_1

###########

def EMA_length = 8;

def AvgExp = ExpAverage(price[-displace], EMA_length);

def condition6_EMA_1 = (price >= AvgExp) and (AvgExp[2] <= AvgExp);

def condition6D_EMA_1 = (price < AvgExp) and (AvgExp[2] > AvgExp);

#############

#EMA_2

#############

def EMA_2length = 20;

def displace2 = 0;

def AvgExp2 = ExpAverage(price[-displace2], EMA_2length);

def condition7_EMA_2 = (price >= AvgExp2) and (AvgExp2[2] <= AvgExp);

def condition7D_EMA_2 = (price < AvgExp2) and (AvgExp2[2] > AvgExp);

##################

#DMI Oscillator

##################

def DMI_length = 5;#Typically set to 10

def diPlus = DMI(DMI_length, DMI_averageType)."DI+";

def diMinus = DMI(DMI_length, DMI_averageType)."DI-";

def Osc = diPlus - diMinus;

def Hist = Osc;

def ZeroLine = 0;

def condition8_DMI = Osc >= ZeroLine;

def condition8D_DMI = Osc < ZeroLine;

###################

#Trend_Periods

###################

def TP_fastLength = 3;#Typically 7

def TP_slowLength = 4;#Typically 15

def Periods = Sign(ExpAverage(close, TP_fastLength) - ExpAverage(close, TP_slowLength));

def condition9_Trend = Periods > 0;

def condition9D_Trend = Periods < 0;

####################################

#Polarized Fractal Efficiency

####################################

def PFE_length = 5;#Typically 10

def smoothingLength = 2.5;#Typically 5

def PFE_diff = close - close[PFE_length - 1];

def val = 100 * Sqrt(Sqr(PFE_diff) + Sqr(PFE_length)) / Sum(Sqrt(1 + Sqr(close - close[1])), PFE_length - 1);

def PFE = ExpAverage(if PFE_diff > 0 then val else -val, smoothingLength);

def UpperLevel = 50;

def LowerLevel = -50;

def condition10_PFE = PFE > 0;

def condition10D_PFE = PFE < 0;

def conditionOB5_PFE = PFE > UpperLevel;

def conditionOS5_PFE = PFE < LowerLevel;

###############################

#Bollinger Bands PercentB

###############################

def BBPB_length = 20;#Typically 20

def Num_Dev_Dn = -2.0;

def Num_Dev_up = 2.0;

def BBPB_OB = 100;

def BBPB_OS = 0;

def upperBand = BollingerBands(price, displace, BBPB_length, Num_Dev_Dn, Num_Dev_up, averagetype).UpperBand;

def lowerBand = BollingerBands(price, displace, BBPB_length, Num_Dev_Dn, Num_Dev_up, averagetype).LowerBand;

def PercentB = (price - lowerBand) / (upperBand - lowerBand) * 100;

def HalfLine = 50;

def UnitLine = 100;

def condition11_BB = PercentB > HalfLine;

def condition11D_BB = PercentB < HalfLine;

def conditionOB6_BB = PercentB > BBPB_OB;

def conditionOS6_BB = PercentB < BBPB_OS;

def condition12_BB = (Upper_BandS[1] <= Upper_BandS) and (Lower_BandS[1] <= Lower_BandS);

def condition12D_BB = (Upper_BandS[1] > Upper_BandS) and (Lower_BandS[1] > Lower_BandS);

#########################

#Klinger Histogram

#########################

def Klinger_Length = 13;

def KVOsc = KlingerOscillator(Klinger_Length).KVOsc;

def KVOH = KVOsc - Average(KVOsc, Klinger_Length);

def condition13_KH = (KVOH > 0);

def condition13D_KH = (KVOH < 0);

#############################

#Projection Oscillator

#############################

def ProjectionOsc_length = 30;#Typically 10

def MaxBound = HighestWeighted(high, ProjectionOsc_length, LinearRegressionSlope(price = high, length = ProjectionOsc_length));

def MinBound = LowestWeighted(low, ProjectionOsc_length, LinearRegressionSlope(price = low, length = ProjectionOsc_length));

def ProjectionOsc_diff = MaxBound - MinBound;

def PROSC = if ProjectionOsc_diff != 0 then 100 * (close - MinBound) / ProjectionOsc_diff else 0;

def PROSC_OB = 80;

def PROSC_OS = 20;

def condition14_PO = PROSC > 50;

def condition14D_PO = PROSC < 50;

def conditionOB7_PO = PROSC > PROSC_OB;

def conditionOS7_PO = PROSC < PROSC_OS;

################

# AK Trend

################

def aktrend_input1 = 3;

def aktrend_input2 = 8;

def aktrend_price = close;

def aktrend_fastmaa = MovAvgExponential(aktrend_price, aktrend_input1);

def aktrend_fastmab = MovAvgExponential(aktrend_price, aktrend_input2);

def aktrend_bspread = (aktrend_fastmaa - aktrend_fastmab) * 1.001;

def cond1_UP_AK = if aktrend_bspread > 0 then 1 else 0;

def cond1_DN_AK = if aktrend_bspread <= 0 then -1 else 0;

#############

# ZSCORE

#############

def zscore_price = close;

def zscore_length = 20;

def zscore_ZavgLength = 20;

def zscore_oneSD = StDev(zscore_price, zscore_length);

def zscore_avgClose = SimpleMovingAvg(zscore_price, zscore_length);

def zscore_ofoneSD = zscore_oneSD * zscore_price[1];

def zscore_Zscorevalue = ((zscore_price - zscore_avgClose) / zscore_oneSD);

def zscore_avgZv = Average(zscore_Zscorevalue, 20);

def zscore_Zscore = ((zscore_price - zscore_avgClose) / zscore_oneSD);

def zscore_avgZscore = Average(zscore_Zscorevalue, zscore_ZavgLength);

def cond2_UP_ZSCORE = if zscore_Zscore > 0 then 1 else 0;

def cond2_DN_ZSCORE = if zscore_Zscore <= 0 then -1 else 0;

############

# Ehlers

############

def ehlers_price = (high + low) / 2;

def ehlers_coeff = ehlers_length * ehlers_price * ehlers_price - 2 * ehlers_price * Sum(ehlers_price, ehlers_length)[1] + Sum(ehlers_price * ehlers_price, ehlers_length)[1];

def Ehlers = Sum(ehlers_coeff * ehlers_price, ehlers_length) / Sum(ehlers_coeff, ehlers_length);

def Ehlers3 = average(Ehlers, elhers3length);

def cond3_UP_Ehlers = if close > Ehlers3 then 1 else 0;

def cond3_DN_Ehlers = if close <= Ehlers3 then -1 else 0;

#########################

# Anchored Momentum

#########################

def amom_src = close;

def amom_MomentumPeriod = 10;

def amom_SignalPeriod = 8;

def amom_SmoothMomentum = no;

def amom_SmoothingPeriod = 7;

def amom_p = 2 * amom_MomentumPeriod + 1;

def amom_t_amom = if amom_SmoothMomentum == yes then ExpAverage(amom_src, amom_SmoothingPeriod) else amom_src;

def amom_amom = 100 * ( (amom_t_amom / ( Average(amom_src, amom_p)) - 1));

def amom_amoms = Average(amom_amom, amom_SignalPeriod);

def cond4_UP_AM = if amom_amom > 0 then 1 else 0;

def cond4_DN_AM = if amom_amom <= 0 then -1 else 0;

#########

# TMO

#########

def tmo_length = 30; #def 14

def tmo_calcLength = 6; #def 5

def tmo_smoothLength = 6; #def 3

def tmo_data = fold i = 0 to tmo_length with s do s + (if close > GetValue(open, i) then 1 else if close < GetValue(open, i) then - 1 else 0);

def tmo_EMA5 = ExpAverage(tmo_data, tmo_calcLength);

def tmo_Main = ExpAverage(tmo_EMA5, tmo_smoothLength);

def tmo_Signal = ExpAverage(tmo_Main, tmo_smoothLength);

def tmo_color = if tmo_Main > tmo_Signal then 1 else -1;

def cond5_UP_TMO = if tmo_Main <= 0 then 1 else 0;

def cond5_DN_TMO = if tmo_Main >= 0 then -1 else 0;

################################

# --- TRIPLE EXHAUSTION ---

################################

def agperiod1 = GetAggregationPeriod();

def over_bought_3x = 80;

def over_sold_3x = 20;

def KPeriod_3x = 10;

def DPeriod_3x = 10;

def priceH1 = high(period = agperiod1);

def priceL1 = low(period = agperiod1);

def priceC1 = close(period = agperiod1);

def priceO1 = close(period = agperiod1);

def priceH_3x = high;

def priceL_3x = low;

def priceC_3x = close;

def SlowK_3x = reference StochasticFull(over_bought_3x, over_sold_3x, KPeriod_3x, DPeriod_3x, priceH_3x, priceL_3x, priceC_3x, 3, averagetype).FullK;

def MACD_3x = reference MACD()."Value";

def priceMean_3x = Average(MACD_3x, length_3x);

def MACD_stdev_3x = (MACD_3x - priceMean_3x) / StDev(MACD_3x, length_3x);

def dPlus_3x = reference DMI()."DI+";

def dMinus_3x = reference DMI()."DI-";

def sellerRegular = SlowK_3x < 20 and MACD_stdev_3x < -1 and dPlus_3x < 15;

def sellerExtreme = SlowK_3x < 20 and MACD_stdev_3x < -2 and dPlus_3x < 15;

def buyerRegular = SlowK_3x > 80 and MACD_stdev_3x > 1 and dMinus_3x < 15;

def buyerExtreme = SlowK_3x > 80 and MACD_stdev_3x > 2 and dMinus_3x < 15;

def ExtremeBuy = if sellerExtreme[1] and !sellerExtreme then 1 else 0;

def ExtremeSell = if buyerExtreme[1] and !buyerExtreme then 1 else 0;

def RegularSell = if buyerRegular[1] and !buyerRegular then 1 else 0;

def RegularBuy= if sellerRegular[1] and !sellerRegular then 1 else 0;

def cond6_UP_Triple_Exh = if sellerRegular or sellerExtreme then 1 else 0;

def cond6_DN_Triple_Exh = if buyerRegular or buyerExtreme then -1 else 0;

###########################

# --- ALERT 4 --- #

###########################

def pd = 22;

def bbl = 20;

def lb = 50;

def ph = 0.85;

def pl = 1.01;

# Downtrend Criterias

def ltLB = 40;

def mtLB = 14;

def str = 3;

def AtrMult_Blst = 1.0;

def nATR_Blst = 4;

def AvgType_Blst = AverageType.HULL;

def ATR = MovingAverage(AvgType, TrueRange(high, close, low), nATR_Blst);

def UP_B = HL2 + (AtrMult * ATR);

def DN = HL2 + (-AtrMult * ATR);

def ST = if close < ST[1] then UP_B else DN;

def SuperTrend = ST;

def val1 = AbsValue(close - open);

def range = high - low;

def blastOffVal = (val1 / range) * 100;

def trigger = trig;

def alert1 = blastOffVal < trig;

def col = blastOffVal < trig;

def blast_candle = blastOffVal < trig;

# Downtrend Criterias

def wvf = ((highest(close, pd) - low) / (highest(close, pd))) * 100;

def sDev = lb * stdev(wvf, bbl);

def midLine1 = SimpleMovingAvg(wvf, bbl);

def lowerBand1 = midLine1 - sDev;

def upperBand1 = midLinE1 + sDev;

def rangeHigh = (highest(wvf, lb)) * ph;

# Filtered Bar Criteria

def upRange = low > low[1] and close > high[1];

def upRange_Aggr = close > close[1] and close > open[1];

def filtered = ((wvf[1] >= upperBand1[1] or wvf[1] >= rangeHigh[1]) and (wvf<upperBand1 and wvf<rangeHigh));

def filtered_Aggr = (wvf[1] >= upperBand1[1] or wvf[1] >= rangeHigh[1]);

# Alerts Criteria 1

def alert4 = upRange_Aggr and close > close[str] and (close < close[ltLB] or close < close[mtLB]) and filtered_Aggr;

def lengthVolAvgPlot = 21;

def VolAvg = Average(volume, lengthVolAvgPlot);

def MA = if type == type.SMP then SimpleMovingAvg(volume, length_HV) else MovAvgExponential(volume, length_HV);

def HighV = if (100 * ((volume / ma) - 1) >= hotPct) then 1 else 0;

def VolAbvAverage = if volume >= VolAvg then 1 else 0;

def Cond_Alert4_UP = if Alert4 within 2 bars then 1 else 0;

#####################

# Market Phases

#####################

def O = open;

def H2 = high;

def C = close;

def L2 = low;

def V = volume;

def SV = V * (H - C) / (H - L);

def BV = V * (C - L) / (H - L);

def fastavg = 50;

def slowavg = 200;

def fastsma = Average( close, fastavg);

def slowsma = Average(close, slowavg);

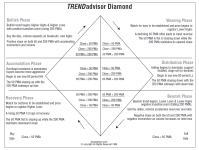

def buystrong = if high > high[1] and low > low[1] and BV*1.05 > SV then 1 else 0;

def cond7_UP_Buystrong = if buystrong then 1 else 0;

def sellstrong = if high < high[1] and low < low[1] and SV*1.05 > BV then 1 else 0;

def cond7_DN_sellstrong = if sellstrong then -1 else 0;

def pricestrong = if high > high[1] and high [1] > high[2] and low > low[1] and low[1] > low[2] then 1 else 0;

def cond8_UP_pricestrong = if pricestrong then 1 else 0;

def priceweak = if high < high[1] and high[1] < high[2] and low < low[1] and low[1] < low[2] then 1 else 0;

def cond8_DN_priceweak = if priceweak then -1 else 0;

def bullphase = fastsma > slowsma && price > fastsma && price > slowsma;

def cond9_UP_bullphase = if bullphase then 1 else 0;

def bearphase = fastsma < slowsma && price < fastsma && price < slowsma;

def cond9_DN_bearphase = if bearphase then -1 else 0;

def accphase = fastsma < slowsma && price > fastsma && price > slowsma;

def cond10_UP_accphase = if accphase then 1 else 0;

def distphase = fastsma > slowsma && price < fastsma && price < slowsma;

def cond10_DN_distphase = if distphase then -1 else 0;

def recphase = fastsma < slowsma && price < slowsma && price > fastsma;

def cond11_UP_recphase = if recphase then 1 else 0;

def warnphase = fastsma > slowsma && price > slowsma && price < fastsma;

###################################

##Big4 Strategy

###################################

def cond_UP = cond1_UP_AK + cond2_UP_ZSCORE + cond3_UP_Ehlers + cond4_UP_AM;

def cond_DN = cond1_DN_AK + cond2_DN_ZSCORE + cond3_DN_Ehlers + cond4_DN_AM;

def direction = if cond_UP >= Strategy_Confirmation_Factor and (!Strategy_FilterWithTMO or cond5_UP_TMO) then 1

else if cond_DN <= -Strategy_Confirmation_Factor and (!Strategy_FilterWithTMO or cond5_DN_TMO) then -1

else if !Strategy_HoldTrend and direction[1] == 1 and cond_UP < Strategy_Confirmation_Factor and cond_DN > -Strategy_Confirmation_Factor then 0

else if !Strategy_HoldTrend and direction[1] == -1 and cond_DN > -Strategy_Confirmation_Factor and cond_UP < Strategy_Confirmation_Factor then 0

else direction[1];

def direction2 = if cond_UP >= Strategy_Confirmation_Factor and (!Strategy_FilterWithTMO_arrows or cond5_UP_TMO) then 1

else if cond_DN <= -Strategy_Confirmation_Factor and (!Strategy_FilterWithTMO_arrows or cond5_DN_TMO) then -1

else if !Strategy_HoldTrend and direction2[1] == 1 and cond_UP < Strategy_Confirmation_Factor and cond_DN > -Strategy_Confirmation_Factor then 0

else if !Strategy_HoldTrend and direction2[1] == -1 and cond_DN > -Strategy_Confirmation_Factor and cond_UP < Strategy_Confirmation_Factor then 0 else direction2[1];

def direction_Equals_zero = direction == 0;

###################################

#Trend Confirmation Calculator

###################################

def Confirmation_Factor = 7;

def Agreement_LevelOB = 12;

def Agreement_LevelOS = 2;

def factorK = 2.0;

def lengthK = 20;

def shift = factorK * MovingAverage(trueRangeAverageType, TrueRange(high, close, low), lengthK);

def averageK = MovingAverage(averageType, price, lengthK);

def AvgK = averageK[-displace];

def Upper_BandK = averageK[-displace] + shift[-displace];

def Lower_BandK = averageK[-displace] - shift[-displace];

def conditionK1UP = price >= Upper_BandK;

def conditionK2UP = (Upper_BandK[1] < Upper_BandK) and (Lower_BandK[1] < Lower_BandK);

def conditionK3DN = (Upper_BandK[1] > Upper_BandK) and (Lower_BandK[1] > Lower_BandK);

def conditionK4DN = price < Lower_BandK;

#######################################################

## AGREEMENT LEVEL

#######################################################

def Agreement_Level = condition1_Yellow_Candle + condition2_RSI + condition3_MFI + condition4_Forcast

+ condition5_CIP + condition6_EMA_1 + condition7_EMA_2 + condition8_DMI + condition9_Trend

+ condition10_PFE + condition11_BB + condition12_BB + condition13_KH + condition14_PO

+ conditionK1UP + conditionK2UP;

def Agreement_LevelD = (condition1D_Yellow_Candle + condition2D_RSI + condition3D_MFI + condition4D_Forcast + condition5D_CIP

+ condition6D_EMA_1 + condition7D_EMA_2 + condition8D_DMI + condition9D_Trend + condition10D_PFE

+ condition11D_BB + condition12D_BB + condition13D_KH + condition14D_PO + conditionK3DN

+ conditionK4DN);

#######################################################

## CONSENSUS LEVEL

#######################################################

def Consensus_Level = Agreement_Level - Agreement_LevelD;

def Consensus_UP = 6;

def Consensus_DOWN = -6;

def UP = Consensus_Level >= Consensus_UP;

def DOWN = Consensus_Level < Consensus_DOWN;

def priceColor = if UP then 1

else if DOWN then -1

else priceColor[1];

def Consensus_Level_OB = 14;

def Consensus_Level_OS = -12;

#Super_OB/OS Signal

def OB_Level = conditionOB1_RSI + conditionOB2_MFI + conditionOB3_Forcast + conditionOB4_Forcast + conditionOB5_PFE + conditionOB6_BB + conditionOB7_PO;

def OS_Level = conditionOS1_RSI + conditionOS2_MFI + conditionOS3_Forcast + conditionOS4_Forcast + conditionOS5_PFE + conditionOS6_BB + conditionOS7_PO;

def Consensus_Line = OB_Level - OS_Level;

input Super_OB = 4;

input Super_OS = -4;

def DOWN_OB = (Agreement_Level > Agreement_LevelOB) and (Consensus_Line > Super_OB) and (Consensus_Level > Consensus_Level_OB);

def UP_OS = (Agreement_Level < Agreement_LevelOS) and (Consensus_Line < Super_OS) and (Consensus_Level < Consensus_Level_OS);

def OS_Buy = UP_OS;

def OB_Sell = DOWN_OB;

def neutral = Consensus_Line < Super_OB and Consensus_Line > Super_OS;

def YHOB = if coloredCandlesOn and ((price1 > Upper_BandS) and (condition_BandRevDn)) then high else Double.NaN;

def YHOS = if coloredCandlesOn and ((price1 < Lower_BandS) and (condition_BandRevUp)) then high else Double.NaN;

def YLOB = if coloredCandlesOn and ((price1 > Upper_BandS) and (condition_BandRevDn)) then low else Double.NaN;

def YLOS = if coloredCandlesOn and ((price1 < Lower_BandS) and (condition_BandRevUp)) then low else Double.NaN;

#extend midline of yellow candle

plot YCOB = if !IsNaN(YHOB) then hl2 else Double.NaN;

YCOB.SetPaintingStrategy(PaintingStrategy.HORIZONTAL);

YCOB.SetDefaultColor(Color.GREEN);

def YHextOB = if IsNaN(YCOB) then YHextOB[1] else YCOB;

plot YHextlineOB = YHextOB;

YHextlineOB.SetPaintingStrategy(PaintingStrategy.HORIZONTAL);

YHextlineOB.SetDefaultColor(Color.ORANGE);

YHextlineOB.SetLineWeight(2);

plot YCOS = if !IsNaN(YHOS) then hl2 else Double.NaN;

YCOS.SetPaintingStrategy(PaintingStrategy.HORIZONTAL);

YCOS.SetDefaultColor(Color.GREEN);

def YHextOS = if IsNaN(YCOS) then YHextOS[1] else YCOS;

plot YHextlineOS = YHextOS;

YHextlineOS.SetPaintingStrategy(PaintingStrategy.HORIZONTAL);

YHextlineOS.SetDefaultColor(Color.LIGHT_GREEN);

YHextlineOS.SetLineWeight(2);

def YC = coloredCandlesOn and priceColor == 1 and price1 > Upper_BandS and condition_BandRevDn;

def HH = Highest(high[1], BarsUsedForRange);

def LL = Lowest(low[1], BarsUsedForRange);

def maxH = Highest(HH, BarsRequiredToRemainInRange);

def maxL = Lowest(LL, BarsRequiredToRemainInRange);

def HHn = if maxH == maxH[1] or maxL == maxL then maxH else HHn[1];

def LLn = if maxH == maxH[1] or maxL == maxL then maxL else LLn[1];

def Bh = if high <= HHn and HHn == HHn[1] then HHn else Double.NaN;

def Bl = if low >= LLn and LLn == LLn[1] then LLn else Double.NaN;

def CountH = if IsNaN(Bh) or IsNaN(Bl) then 2 else CountH[1] + 1;

def CountL = if IsNaN(Bh) or IsNaN(Bl) then 2 else CountL[1] + 1;

def ExpH = if BarNumber() == 1 then Double.NaN else

if CountH[-BarsRequiredToRemainInRange] >= BarsRequiredToRemainInRange then HHn[-BarsRequiredToRemainInRange] else

if high <= ExpH[1] then ExpH[1] else Double.NaN;

def ExpL = if BarNumber() == 1 then Double.NaN else

if CountL[-BarsRequiredToRemainInRange] >= BarsRequiredToRemainInRange then LLn[-BarsRequiredToRemainInRange] else

if low >= ExpL[1] then ExpL[1] else Double.NaN;

def BoxHigh = if ((DOWN_OB) or (Upper_BandS crosses above Upper_BandK2) or (condition_BandRevDn) and (high > high[1]) and ((price > Upper_BandK2) or (price > Upper_BandS))) then Highest(ExpH) else Double.NaN;

def BoxLow = if (DOWN_OB) or ((Upper_BandS crosses above Upper_BandK2)) then Lowest(low) else Double.NaN;

def BoxHigh2 = if ((UP_OS) or ((Lower_BandS crosses below Lower_BandK2))) then Highest(ExpH) else Double.NaN;

def BH2 = if !IsNaN(BoxHigh2) then high else Double.NaN;

def BH2ext = if IsNaN(BH2) then BH2ext[1] else BH2;

def BH2extline = BH2ext;

def H_BH2extline2 = Lowest(BH2extline, 1);

def BoxLow2 = if ((UP_OS) or (Lower_BandS crosses below Lower_BandK2) or (condition_BandRevUp) and (low < low[1]) and ((price < Lower_BandK2) or (price < Lower_BandS))) or ((UP_OS[1]) and (low < low[1])) then Lowest(low) else Double.NaN;

def BH1 = if !IsNaN(BoxHigh) then high else Double.NaN;

def BH1ext = if IsNaN(BH1) then BH1ext[1] else BH1;

def BH1extline = BH1ext;

def BL1 = if !IsNaN(BoxLow) then low else Double.NaN;

def BL1ext = if IsNaN(BL1) then BL1ext[1] else BL1;

## HORIZONTAL RED AND GREEN ZONE LINES

def BL1extline2 = BL1ext;

def BL2 = if !IsNaN(BoxLow2) then low else Double.NaN;

def BL2ext = if IsNaN(BL2) then BL2ext[1] else BL2;

def BL2extline2 = BL2ext;

def KeylevelOB = if ((BH1ext >= YHextlineOB) and (BL1ext <= YHextlineOB))then 1 else 0;

def KeylevelOS = if ((BH2ext >= YHextlineOS) and (BL2ext <= YHextlineOS))then 1 else 0;

## RED AND GREEN ZONE WHEN STEPPING DOWN

plot H_BH2extline = Lowest(BH2extline, 1);

H_BH2extline.SetDefaultColor(Color.dark_GREEN);

plot BL1extline = BL1ext;

BL1extline.SetPaintingStrategy(PaintingStrategy.HORIZONTAL);

BL1extline.SetDefaultColor(Color.dark_RED);

BL1extline.SetLineWeight(1);

plot BL2extline = BL2ext;

BL2extline.SetPaintingStrategy(PaintingStrategy.HORIZONTAL);

BL2extline.SetDefaultColor(Color.dark_GREEN);

BL2extline.SetLineWeight(1);

plot H_BH1extline = Highest(BH1extline, 1);

H_BH1extline.SetDefaultColor(Color.dark_RED);

plot L_BL1extline = Highest(BL1extline, 1);

L_BL1extline.SetDefaultColor(Color.dark_RED);

plot L_BL2extline = Lowest(BL2extline, 1);

L_BL2extline.SetDefaultColor(Color.dark_GREEN);

############################################################

AddCloud(if !HideCloud then BH1extline else Double.NaN, BL1extline, Color.DARK_RED, Color.GRAY);

AddCloud(if !HideCloud then BH2extline else Double.NaN, BL2extline, Color.DARK_GREEN, Color.GRAY);

############################################################

##C3_MF_Line_v2 Created by Christopher84 03/06/2022

############################################################

script WMA_Smooth {

input price_WMA = hl2;

plot smooth = (4 * price_WMA

+ 3 * price_WMA[1]

+ 2 * price_WMA[2]

+ price_WMA[3]) / 10;

}

script Phase_Accumulation {

# This is Ehler's Phase Accumulation code. It has a full cycle delay.

# However, it computes the correction factor to a very high degree.

input price_WMA = hl2;

rec Smooth;

rec Detrender;

rec Period;

rec Q1;

rec I1;

rec I1p;

rec Q1p;

rec Phase1;

rec Phase;

rec DeltaPhase;

rec DeltaPhase1;

rec InstPeriod1;

rec InstPeriod;

def CorrectionFactor;

if BarNumber() <= 5

then {

Period = 0;

Smooth = 0;

Detrender = 0;

CorrectionFactor = 0;

Q1 = 0;

I1 = 0;

Q1p = 0;

I1p = 0;

Phase = 0;

Phase1 = 0;

DeltaPhase1 = 0;

DeltaPhase = 0;

InstPeriod = 0;

InstPeriod1 = 0;

} else {

CorrectionFactor = 0.075 * Period[1] + 0.54;

# Smooth and detrend my smoothed signal:

Smooth = WMA_Smooth(price_WMA);

Detrender = ( 0.0962 * Smooth

+ 0.5769 * Smooth[2]

- 0.5769 * Smooth[4]

- 0.0962 * Smooth[6] ) * CorrectionFactor;

# Compute Quadrature and Phase of Detrended signal:

Q1p = ( 0.0962 * Detrender

+ 0.5769 * Detrender[2]

- 0.5769 * Detrender[4]

- 0.0962 * Detrender[6] ) * CorrectionFactor;

I1p = Detrender[3];

# Smooth out Quadrature and Phase:

I1 = 0.15 * I1p + 0.85 * I1p[1];

Q1 = 0.15 * Q1p + 0.85 * Q1p[1];

# Determine Phase

if I1 != 0

then {

# Normally, ATAN gives results from -pi/2 to pi/2.

# We need to map this to circular coordinates 0 to 2pi

if Q1 >= 0 and I1 > 0

then { # Quarant 1

Phase1 = ATan(AbsValue(Q1 / I1));

} else if Q1 >= 0 and I1 < 0

then { # Quadrant 2

Phase1 = Double.Pi - ATan(AbsValue(Q1 / I1));

} else if Q1 < 0 and I1 < 0

then { # Quadrant 3

Phase1 = Double.Pi + ATan(AbsValue(Q1 / I1));

} else { # Quadrant 4

Phase1 = 2 * Double.Pi - ATan(AbsValue(Q1 / I1));

}

} else if Q1 > 0

then { # I1 == 0, Q1 is positive

Phase1 = Double.Pi / 2;

} else if Q1 < 0

then { # I1 == 0, Q1 is negative

Phase1 = 3 * Double.Pi / 2;

} else { # I1 and Q1 == 0

Phase1 = 0;

}

# Convert phase to degrees

Phase = Phase1 * 180 / Double.Pi;

if Phase[1] < 90 and Phase > 270

then {

# This occurs when there is a big jump from 360-0

DeltaPhase1 = 360 + Phase[1] - Phase;

} else {

DeltaPhase1 = Phase[1] - Phase;

}

# Limit our delta phases between 7 and 60

if DeltaPhase1 < 7

then {

DeltaPhase = 7;

} else if DeltaPhase1 > 60

then {

DeltaPhase = 60;

} else {

DeltaPhase = DeltaPhase1;

}

# Determine Instantaneous period:

InstPeriod1 =

-1 * (fold i = 0 to 40 with v=0 do

if v < 0 then

v

else if v > 360 then

-i

else

v + GetValue(DeltaPhase, i, 41));

if InstPeriod1 <= 0

then {

InstPeriod = InstPeriod[1];

} else {

InstPeriod = InstPeriod1;

}

Period = 0.25 * InstPeriod + 0.75 * Period[1];

}

plot DC = Period;

}

script Ehler_MAMA {

input price_WMA = hl2;

input FastLimit = 0.5;

input SlowLimit = 0.05;

rec Period;

rec Period_raw;

rec Period_cap;

rec Period_lim;

rec Smooth;

rec Detrender;

rec I1;

rec Q1;

rec jI;

rec jQ;

rec I2;

rec Q2;

rec I2_raw;

rec Q2_raw;

rec Phase;

rec DeltaPhase;

rec DeltaPhase_raw;

rec alpha;

rec alpha_raw;

rec Re;

rec Im;

rec Re_raw;

rec Im_raw;

rec SmoothPeriod;

rec vmama;

rec vfama;

def CorrectionFactor = Phase_Accumulation(price_WMA).CorrectionFactor;

if BarNumber() <= 5

then {

Smooth = 0;

Detrender = 0;

Period = 0;

Period_raw = 0;

Period_cap = 0;

Period_lim = 0;

I1 = 0;

Q1 = 0;

I2 = 0;

Q2 = 0;

jI = 0;

jQ = 0;

I2_raw = 0;

Q2_raw = 0;

Re = 0;

Im = 0;

Re_raw = 0;

Im_raw = 0;

SmoothPeriod = 0;

Phase = 0;

DeltaPhase = 0;

DeltaPhase_raw = 0;

alpha = 0;

alpha_raw = 0;

vmama = 0;

vfama = 0;

} else {

# Smooth and detrend my smoothed signal:

Smooth = WMA_Smooth(price_WMA);

Detrender = ( 0.0962 * Smooth

+ 0.5769 * Smooth[2]

- 0.5769 * Smooth[4]

- 0.0962 * Smooth[6] ) * CorrectionFactor;

Q1 = ( 0.0962 * Detrender

+ 0.5769 * Detrender[2]

- 0.5769 * Detrender[4]

- 0.0962 * Detrender[6] ) * CorrectionFactor;

I1 = Detrender[3];

jI = ( 0.0962 * I1

+ 0.5769 * I1[2]

- 0.5769 * I1[4]

- 0.0962 * I1[6] ) * CorrectionFactor;

jQ = ( 0.0962 * Q1

+ 0.5769 * Q1[2]

- 0.5769 * Q1[4]

- 0.0962 * Q1[6] ) * CorrectionFactor;

# This is the complex conjugate

I2_raw = I1 - jQ;

Q2_raw = Q1 + jI;

I2 = 0.2 * I2_raw + 0.8 * I2_raw[1];

Q2 = 0.2 * Q2_raw + 0.8 * Q2_raw[1];

Re_raw = I2 * I2[1] + Q2 * Q2[1];

Im_raw = I2 * Q2[1] - Q2 * I2[1];

Re = 0.2 * Re_raw + 0.8 * Re_raw[1];

Im = 0.2 * Im_raw + 0.8 * Im_raw[1];

# Compute the phase

if Re != 0 and Im != 0

then {

Period_raw = 2 * Double.Pi / ATan(Im / Re);

} else {

Period_raw = 0;

}

if Period_raw > 1.5 * Period_raw[1]

then {

Period_cap = 1.5 * Period_raw[1];

} else if Period_raw < 0.67 * Period_raw[1] {

Period_cap = 0.67 * Period_raw[1];

} else {

Period_cap = Period_raw;

}

if Period_cap < 6

then {

Period_lim = 6;

} else if Period_cap > 50

then {

Period_lim = 50;

} else {

Period_lim = Period_cap;

}

Period = 0.2 * Period_lim + 0.8 * Period_lim[1];

SmoothPeriod = 0.33 * Period + 0.67 * SmoothPeriod[1];

if I1 != 0

then {

Phase = ATan(Q1 / I1);

} else if Q1 > 0

then { # Quadrant 1:

Phase = Double.Pi / 2;

} else if Q1 < 0

then { # Quadrant 4:

Phase = -Double.Pi / 2;

} else { # Both numerator and denominator are 0.

Phase = 0;

}

DeltaPhase_raw = Phase[1] - Phase;

if DeltaPhase_raw < 1

then {

DeltaPhase = 1;

} else {

DeltaPhase = DeltaPhase_raw;

}

alpha_raw = FastLimit / DeltaPhase;

if alpha_raw < SlowLimit

then {

alpha = SlowLimit;

} else {

alpha = alpha_raw;

}

vmama = alpha * price_WMA + (1 - alpha) * vmama[1];

vfama = 0.5 * alpha * vmama + (1 - 0.5 * alpha) * vfama[1];

}

plot MAMA = vmama;

plot FAMA = vfama;

}

def price2 = hl2;

def FastLimit = 0.5;

def SlowLimit = 0.05;

def MAMA = Ehler_MAMA(price2, FastLimit, SlowLimit).MAMA;

def FAMA = Ehler_MAMA(price2, FastLimit, SlowLimit).FAMA;

def Crossing = Crosses((MAMA < FAMA), yes);

def Crossing1 = Crosses((MAMA > FAMA), yes);

def C3_Line_1 = if ((priceColor == 1) and (price1 > Upper_BandS) and (condition_BandRevDn)) then 1 else 0;

def C3_Line_2 = if ((priceColor == -1) and (price1 < Lower_BandS) and (condition_BandRevUp)) then 1 else 0;

def C3_Green = ((priceColor == 1));

def C3_red = ((priceColor == 1));

AddLabel(yes, Concat("MAMA", Concat("",

if MAMA > FAMA then "" else "")),

if MAMA > FAMA then Color.LIGHT_GREEN else Color.red);

def MF_UP = FAMA < MAMA;

def MF_DN = FAMA > MAMA;

def Cond12_MF_UP = MF_DN[1] and !MF_DN;

def Cond12_MF_DN = MF_UP[1] and !MF_UP;

def priceColor10_MF = if MF_UP then 1

else if MF_DN then -1

else priceColor10_MF[1];

###################################

##Consensus Level & Squeeze Label

###################################

def MomentumUP = Consensus_Level[1] < Consensus_Level;

def MomentumDOWN = Consensus_Level[1] > Consensus_Level;

def conditionOB_CL = (Consensus_Level >= 12) and (Consensus_Line >= 4);

def conditionOS_CL = (Consensus_Level <= -12) and (Consensus_Line <= -3);

###################################

#SPARK#

###################################

def AvgExp8 = ExpAverage(price[-displace], length8);

def UPD = AvgExp8[1] < AvgExp8;

def AvgExp9 = ExpAverage(price[-displace], length9);

def UPW = AvgExp9[1] < AvgExp9;

def Below = AvgExp8 < AvgExp9;

def Spark = UPD + UPW + Below;

def UPEMA = AvgExp8[1] < AvgExp8;

def DOWNEMA = AvgExp8[1] > AvgExp8;

def BigUP = direction == 1;

def BigDN = direction == -1;

def BigNa = direction == 0;

def UPEMA2 = AvgExp9[1] < AvgExp9;

def DOWNEMA2 = AvgExp9[1] > AvgExp9;

def UP8 = UPEMA and UPEMA2;

def DOWN8 = DOWNEMA and DOWNEMA2;

def priceColor8 = if UP8 then 1

else if DOWN8 then -1

else 0;

def UP11 = UPEMA;

def DOWN11 = DOWNEMA;

def priceColor11 = if UP11 then 1

else if DOWN11 then -1

else 0;

def UP12 = UPEMA2;

def DOWN12 = DOWNEMA2;

def priceColor12 = if UP12 then 1

else if DOWN12 then -1

else 0;

def UpCalc = (priceColor == 1) + (priceColor == 1) + (priceColor8 == 1) + (priceColor10_MF == 1);

def StrongUpCalc = (priceColor == 1) + (priceColor == 1) + (priceColor10_MF == 1);

def CandleColor = if (priceColor == 1) and (priceColor12 == 1) and (Spark >= 2) then 1 else

if (priceColor == -1) and (Spark < 1) then -1 else 0;

def SparkUP1 = (Spark == 3) and (CandleColor == 1);

def SparkDN1 = (Spark == 0) and (CandleColor == -1);

def hide_SparkUP = if SparkUP1 and (SparkUP1[1] or SparkUP1[2] or SparkUP1[3] or SparkUP1[4] or SparkUP1[5]) or (bigdn) then 0 else 1;

def hide_SparkDN = if SparkDN1 and (SparkDN1[1] or SparkDN1[2] or SparkDN1[3] or SparkDN1[4] or SparkDN1[5]) or (bigup) then 0 else 1;

def timeframe = if agperiod1 <= aggregationperiod.DAY then aggregationperiod.DAY else agperiod1;

def Vol = volume(period = timeframe);

def at_High = high(period = timeframe);

def at_Open = open(period = timeframe);

def at_Close = close(period = timeframe);

def at_Low = low(period = timeframe);

def Buy_Volume = RoundUp(Vol * (at_Close - at_Low) / (at_High - at_Low));

def Buy_percent = RoundUp((Buy_Volume / Vol) * 100);

def Sell_Volume = RoundDown(Vol * (at_High - at_Close) / (at_High - at_Low));

def Sell_percent = RoundUp((Sell_Volume / Vol) * 100);

def buying = V*(C-L2)/(H2-L2);

def selling = V*(H2-C)/(H2-L2);

def SellVolPercent = Round((Selling / V) * 100, 0);

def buyVolPercent = Round((Buying / V) * 100, 0);

def SellVol = selling;

def TV = volume;

def BuyVol = buying;

def percentdiff = (SellVolPercent - buyVolPercent);

def percentdiffAbs = absValue(percentdiff);

def horsebull = (buying > selling) and (percentdiffabs >= ControlPercent);

def horsebear = (selling > buying) and (percentdiffabs >= ControlPercent);

def avg1 = ExpAverage(close(period = agperiod1), length8);

def height = avg1 - avg1[length8];

def UP1 = avg1[1] < avg1;

def DOWN1 = avg1[1] > avg1;

def avg2 = ExpAverage(close(period = agperiod1), length8);

#Label color

def Condition1UP = avg1 > avg2;

def Condition1DN = avg1 < avg2;

def Condition2UP = Buy_percent > 50;

def Condition2DN = Buy_percent < 50;

def Condition3UP = if buyerRegular then 1 else 0;

def Condition3DN = if sellerRegular then 1 else 0;

def Condition4UP = if buyerExtreme then 1 else 0;

def Condition4DN = if sellerExtreme then 1 else 0;

###################################################################

def priceColor1 = if ((avg1[1]<avg1) and (avg2[1]<avg2)) then 1 else if((avg1[1]>avg1) and (avg2[1]>avg2)) then -1 else priceColor[1];

def keyobpaint = (hl2 < BH1ext) and (hl2 > BL1ext);

def keyospaint = (hl2 < BH2ext) and (hl2 > BL2ext);

def Alert4_UP_Condition = Use_Alert4_UP_C and alert4;

def Alert4_DN_Condition = Use_Alert4_DN_C and alert4;

def signal_UP_Condition = Use_signal_UP_C and (direction == 1 and direction[1] < 1);

def signal_DN_Condition = Use_signal_DN_C and (direction == -1 and direction[1] > -1);

def signal_2_UP_Condition = Use_signal_2_UP_C and (direction2 == 1 and direction2[1] < 1);

def signal_2_DN_Condition = Use_signal_2_DN_C and (direction2 == -1 and direction2[1] > -1);

def Spark_UP_Condition = Use_Spark_UP_C and (SparkUP1);

def Spark_DN_Condition = Use_Spark_DN_C and (SparkDN1);

def Spark_UP2_Condition = Use_Spark_UP2_C and (SparkUP1) and hide_SparkUP;

def Spark_DN2_Condition = Use_Spark_DN2_C and (SparkDN1) and hide_SparkDN;

def TS_UP_Condition = Use_TS_UP_C and upsignal;

def TS_DN_Condition = Use_TS_DN_C and downsignal;

def TripleExhaustion_UP_Condition = Use_TripleEx_UP_C and RegularBuy or Extremebuy;

def TripleExhaustion_DN_Condition = Use_TripleEx_DN_C and RegularSell or ExtremeSell;

###################################

##

###################################

###################################

## Candle Color

###################################

AssignPriceColor(if Strategy_ColoredCandlesOn then

if ALERT4 THEN COLOR.green

else if Color_3x and buyerRegular then Color.green

else if Color_3xt and buyerExtreme then Color.green

else if Color_3x and buyerRegular[1] then Color.red

else if Color_3xt and buyerExtreme[1] then Color.red

else if direction == 1 then Color.light_green

else if Color_3x and sellerRegular then Color.dark_red

else if Color_3xt and sellerExtreme then Color.Dark_red

else if Color_3x and sellerRegular[1] then Color.green

else if Color_3xt and sellerExtreme[1] then Color.green

else if direction == -1 then color.red

else if direction == 0 then Color.gray

else Color.GRAY

else Color.CURRENT);

####################################################################################################

## Conditions

####################################################################################################

def CloudConditionGreen = EMADaboveZero +

keyobpaint +

topBandStepUp_EMAD +

toppushline +

BottomBandStepup_EMAD +

horsebull +

bullphase +

crossesUpline_EMAD +

MF_UP;

###################################

##

###################################

def CloudConditionRed = EMADbelowZero +

keyospaint +

topBandStepDown_EMAD +

bottompushline +

BottomBandStepdown_EMAD +

horsebear +

bearphase +

crossesDownline_EMAD +

MF_DN;

###################################

##

###################################

def ALLup = if use_EMAD_filter and EMADaboveZero then Alert4_UP_Condition +

signal_UP_Condition +

signal_2_UP_Condition +

Spark_UP_Condition +

Spark_UP2_Condition +

cond6_UP_Triple_Exh +

cond7_UP_Buystrong +

cond8_UP_pricestrong +

cond9_UP_bullphase +

cond10_UP_accphase +

cond11_UP_recphase +

Cond12_MF_UP +

cond13_TS_Buy +

Key_OS_Condition

else if use_EMAD_filter == no then Alert4_UP_Condition +

signal_UP_Condition +

signal_2_UP_Condition +

Spark_UP_Condition +

Spark_UP2_Condition +

cond6_UP_Triple_Exh +

cond7_UP_Buystrong +

cond8_UP_pricestrong +

cond9_UP_bullphase +

cond10_UP_accphase +

cond11_UP_recphase +

Cond12_MF_UP +

cond13_TS_Buy +

Key_OS_Condition

else double.nan;

###################################

##

###################################

def ALLdown = if use_EMAD_filter and EMADbelowZero then Alert4_DN_Condition +

signal_DN_Condition +

signal_2_DN_Condition +

Spark_DN_Condition +

Spark_DN2_Condition +

cond6_DN_Triple_Exh +

cond7_DN_sellstrong +

cond8_DN_priceweak +

cond9_DN_bearphase +

cond10_DN_distphase +

cond11_UP_recphase +

Cond12_MF_DN +

cond13_TS_Sell +

Key_OB_Condition

else if use_EMAD_filter == no then Alert4_DN_Condition +

signal_DN_Condition +

signal_2_DN_Condition +

Spark_DN_Condition +

Spark_DN2_Condition +

cond6_DN_Triple_Exh +

cond7_DN_sellstrong +

cond8_DN_priceweak +

cond9_DN_bearphase +

cond10_DN_distphase +

cond11_UP_recphase +

Cond12_MF_DN +

cond13_TS_Sell +

Key_OB_Condition

else double.nan;

###################################

##

###################################

plot Ehlers_1 = Ehlers3;

Ehlers_1.SetStyle(Curve.SHORT_DASH);

Ehlers_1.SetLineWeight(1);

Ehlers_1.AssignValueColor(if CloudConditionred == CloudConditionGreen then color.gray

else if CloudConditionGreen > Cloud_filter then color.green

else if CloudConditionred > Cloud_filter then color.red

else color.gray);

###################################

##

###################################

plot Squeeze_Alert = sqzLevel;

Squeeze_Alert.SetPaintingStrategy(PaintingStrategy.POINTS);

Squeeze_Alert.SetLineWeight(3);

Squeeze_Alert.AssignValueColor(if(direction2 == 1) then color.yellow

else if direction2 == -1 then color.yellow

else if direction2 == 0 then color.white

else color.yellow);

###################################

##

###################################

plot UpArrow_1 = if Use_Arrow_Inputs and Allup > Arrow_filter then low else double.nan;

UpArrow_1.SetPaintingStrategy(PaintingStrategy.BOOLEAN_ARROW_UP);

UpArrow_1.AssignValueColor(color.green);

UpArrow_1.SetLineWeight(1);

plot DownArrow_1 = if Use_Arrow_Inputs and Alldown > Arrow_filter then high else double.nan;

DownArrow_1.SetPaintingStrategy(PaintingStrategy.BOOLEAN_ARROW_Down);

DownArrow_1.AssignValueColor(color.red);

DownArrow_1.SetLineWeight(1);

###################################

##Labels

###################################

def Buy = UP_OS;

def Sell = DOWN_OB;

def conditionLTB = (conditionK2UP and (Consensus_Level < 0));

def conditionLTS = (conditionK3DN and (Consensus_Level > 0));

def conditionBO = ((Upper_BandS[1] < Upper_BandS))

and ((Lower_BandS[1] < Lower_BandS))

and ((Upper_BandK[1] < Upper_BandK))

and ((Lower_BandK[1] < Lower_BandK));

def conditionBD = ((Upper_BandS[1] > Upper_BandS))

and ((Lower_BandS[1] > Lower_BandS))

and ((Upper_BandK[1] > Upper_BandK))

and ((Lower_BandK[1] > Lower_BandK));

AddLabel(yes, if conditionLTB then "LOOK TO BUY"

else if conditionLTS then "LOOK TO SELL"

else if conditionK2UP then "TREND: BULL"

else if conditionK3DN then "TREND: BEAR" else "TREND: CONSOLIDATION",

if conditionLTB then Color.YELLOW

else if conditionLTS then Color.YELLOW

else if conditionK2UP then Color.LIGHT_GREEN

else if conditionK3DN then Color.RED else Color.GRAY);

AddLabel(yes, if conditionBD then "BREAKDOWN"

else if conditionBO then "BREAKOUT" else "NO BREAK",

if conditionBD then Color.RED

else if conditionBO then Color.GREEN else Color.GRAY);

AddLabel(showLabels, if (Spark == 3) then "SPARK: " + Round(Spark, 1)

else if (Spark == 0) then "SPARK: " + Round(Spark, 1) else "SPARK: " + Round(Spark, 1),

if (Spark == 3) then Color.orange

else if (Spark == 2) then Color.light_GREEN

else if (Spark == 0) then Color.RED else Color.GRAY);

AddLabel(showlabels, if Condition1UP==1 and Condition2UP == 1 and (Condition3UP == 1 or Condition4UP == 1) then "**CALLS ONLY!**"

else if Condition1UP == 1 and Condition2UP == 1 then "VERY BULLISH"

else if direction == 1 then "BULLISH"

else if Condition1DN == 1 and Condition2DN == 1 and (Condition3DN == 1 or Condition4DN == 1) then "**PUTS ONLY!**"

else if Condition1DN == 1 and Condition2DN == 1 then "VERY BEARISH"

else if direction == -1 then "BEARISH"

else if ((avg[1] > avg) and (avg > avg2) and (Buy_percent > 50)) then "BULLISH RETRACEMENT"

else if ((avg[1] < avg) and (avg < avg2) and (Buy_percent < 50)) then "BEARISH RETRACEMENT" else "CHOP",

if Condition1UP == 1 and Condition2UP == 1 and (Condition3UP == 1 or Condition4UP == 1) then Color.cyan

else if Condition1DN == 1 and Condition2DN == 1 and (Condition3DN == 1 or Condition4DN == 1) then Color.Magenta

else if Condition1UP == 1 and Condition2UP == 1 then Color.light_GREEN

else if direction == 1 then Color.light_green

else if Condition1DN == 1 and Condition2DN == 1 then Color.RED

else if direction == -1 then Color.red

else Color.orange);

AddLabel(yes, if MomentumUP then "Consensus Increasing = " + Round(Consensus_Level, 1) else if MomentumUP or MomentumDOWN and conditionOB_CL then "Consensus OVERBOUGHT = " + Round(Consensus_Level, 1) else if MomentumDOWN then "Consensus Decreasing = " + Round(Consensus_Level, 1) else if MomentumUP or MomentumDOWN and conditionOS_CL then "Consensus OVERSOLD = " + Round(Consensus_Level, 1) else "Consensus = " + Round(Consensus_Level, 1), if conditionOB_CL then Color.light_green else if conditionOS_CL then Color.red else Color.GRAY);

AddLabel(squeeze_Alert, "SQUEEZE ALERT", if Squeeze_Alert then Color.YELLOW else Color.GRAY);

def ag = getaggregationPeriod();

def agcondition = if ag >= aggregationPeriod.DAY then 0 else 1;

AddVerticalLine(showverticallineday and agcondition and( GetDay() <> GetDay()[1]), "", Color.dark_gray, Curve.SHORT_DASH);

def Keylevel2OB = (round(absvalue(close - yhextlineOB),1));

def Keylevel2OS = (round(absvalue(close - yhextlineOS),1));

def lengthHLOSOB = 1000;

def HighestKeyOB = highest(yhextlineOB, LengthHLOSOB);

def LowestKeyOS = lowest(yhextlineOS, LengthHLOSOB);

def gethighestKeyOB = if KeylevelOB then HighestKeyOB else double.nan;

def getLowestKeyOS = if KeylevelOB then LowestKeyOS else double.nan;

def Keylevel2cond = if KeylevelOS and (Keylevel2OS < Keylevel2OB) and (Keylevel2OS < control) then 1

else if KeylevelOB and (Keylevel2OB < Keylevel2OS) and (Keylevel2OB < control) then -1 else 0;

AddLabel(KeylevelOS and keyospaint," Near Key Support Level: $" + round(yhextlineOS,0), color.light_green);

AddLabel(KeylevelOB and keyobpaint," Near Key Resistance Level: $" + round(yhextlineOB,0), color.orange);

AddLabel(show_TS_lastlabel,

if TS_Last == 1 then " TS Last Signal: BUY "

else if TS_Last == 0 and ((alert4 or regularBuy or extremebuy) within 5 bars) then " TS Last Signal: SELL "

else if TS_Last == 0 then " TS Last Signal: SELL "

else "",

if TS_Last == 1 then color.light_gray

else if TS_Last == 0 and((alert4 or regularBuy or extremebuy) within 5 bars) then color.orange

else if TS_Last == 0 then color.light_gray

else color.white);

#AddLabel(buystrong, "Buyer Vol Strong ", if buystrong then Color.GREEN else color.black);

#AddLabel(sellstrong, "Seller Vol Strong", if sellstrong then Color.MAGENTA else color.black);

#AddLabel(pricestrong, "Price Strong ", if pricestrong then Color.GREEN else color.black);

#AddLabel(priceweak, "Price Weak", if priceweak then Color.MAGENTA else color.black);

#AddLabel(bullphase, " Bull Phase" , if bullphase is true then Color.GREEN else Color.BLACk);

#AddLabel(accphase, " Accumation Phase ", if accphase is true then Color.lIGHT_GREEN else Color.BLACK);

#AddLabel(recphase, " Recovery Phase ", if recphase is true then Color.lIGHT_ORANGE else Color.BLACK);

#AddLabel(warnphase, " Warning Phase ", if warnphase is true then Color.orANGE else Color.BLACK);

#AddLabel(distphase, " Distribution Phase ", if distphase is true then Color.light_red else Color.BLACK);

#AddLabel(bearphase, " Bear Phase ", if bearphase is true then Color.red else Color.BLACK);

addlabel(yes, " Arrow Filter: " + Arrow_filter, color.white);

#addlabel(yes, " Cloud Filter: " + cloud_filter + " | " + "Up: " + cloudconditionGreen + " | " + "Down: " + cloudconditionred, color.white);

addlabel(yes, if use_EMAD_filter then " EMAD Filter: ON " else if !use_EMAD_filter then " EMAD Filter: OFF " else "", if EMADaboveZero then color.green else if EMADbelowZero then color.red else color.gray);

####################################################################################################

## C3 EMA Cloud

####################################################################################################

AddCloud(if ShowEMAcloud and (AvgExp9 > AvgExp8) then AvgExp9 else Double.NaN, AvgExp8, Createcolor(0,0,0), Color.CURRENT);

AddCloud(if ShowEMAcloud and (AvgExp8 > AvgExp9) then AvgExp8 else Double.NaN, AvgExp9, Createcolor(0,60,0), Color.CURRENT);

###################################

## EMAD Condition Cloud

###################################

AddCloud(if Show_filter_Cloud and (CloudConditionGreen > Cloud_filter) then ehlers3 else Double.NaN, ehlers, color.green, color.dark_green);

AddCloud(if Show_filter_Cloud and (CloudConditionRed > Cloud_filter) then ehlers else Double.NaN, ehlers3, color.red, color.dark_red);

#####################################################################################################################################################################################

")