G

guest

Guest

Hey @Christopher84!

I found one of your previous confirmation candle scripts here:

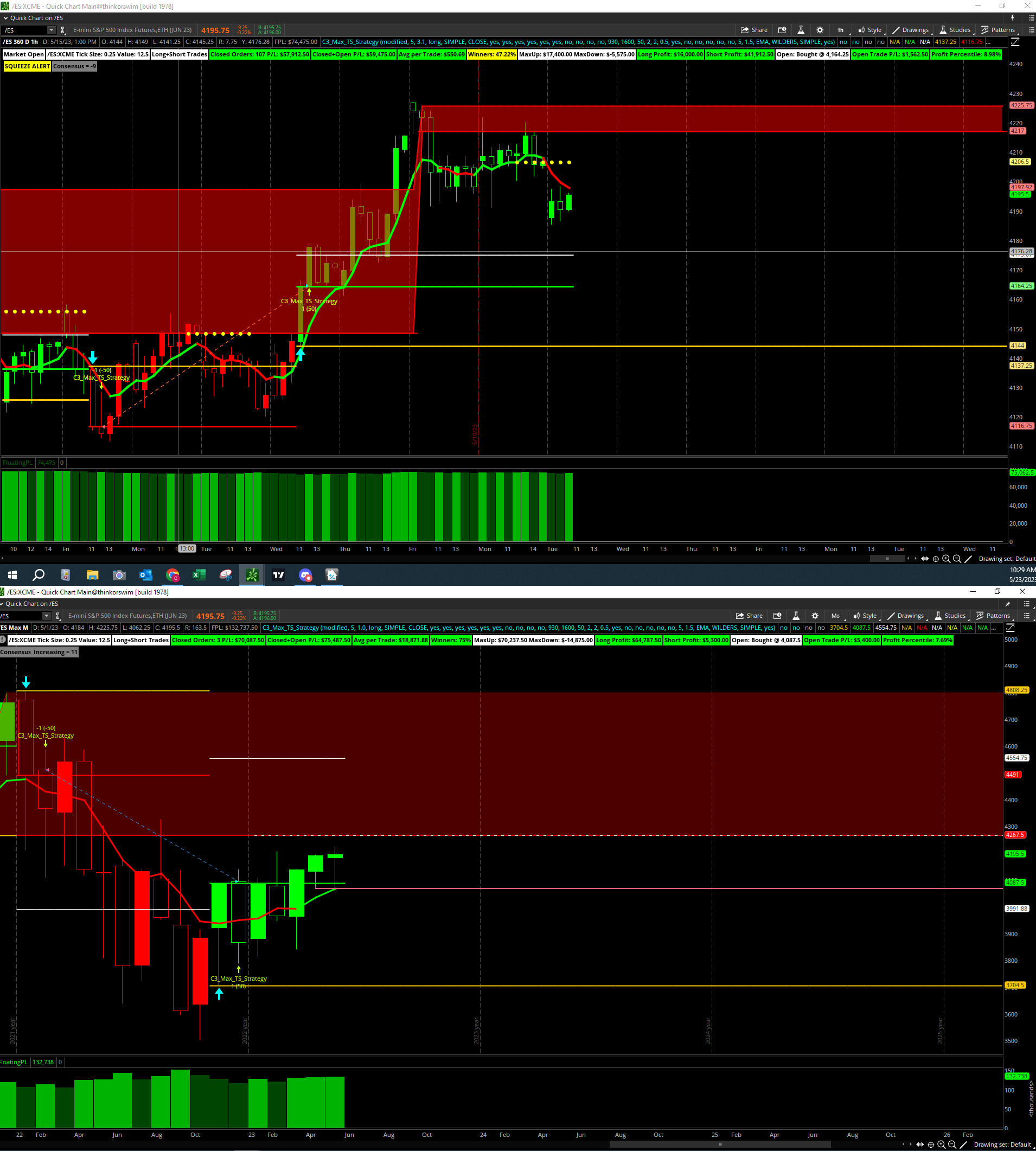

Looks interesting on overbought and oversold zones on a 5 minute and 1 minute chart.

Are you still using this. What do the large and smaller arrows represent and also wanted to know if it repaints?

#Confirmation Candles developed 04/15/2021 by Christopher Wilson

#Select the level of agreement among the 13 indicators included.

#MACD with Price

declare upper;

def price = close;

def fastLength = 12;

def slowLength = 26;

def MACDLength = 9;

input MACD_AverageType = {SMA, default EMA};

def MACDLevel = 0.0;

def fastEMA = ExpAverage(price, fastLength);

def slowEMA = ExpAverage(price, slowLength);

def Value;

def Avg;

switch (MACD_AverageType) {

case SMA:

Value = Average(price, fastLength) - Average(price, slowLength);

Avg = Average(Value, MACDLength);

case EMA:

Value = fastEMA - slowEMA;

Avg = ExpAverage(Value, MACDLength);}

def Diff = Value - Avg;

def Level = MACDLevel;

def condition1 = Value >= MACDLevel;

#RSI

input RSI_length = 14;

input RSI_AverageType = AverageType.WILDERS;

def NetChgAvg = MovingAverage(RSI_AverageType, price - price[1], RSI_length);

def TotChgAvg = MovingAverage(RSI_AverageType, AbsValue(price - price[1]), RSI_length);

def ChgRatio = if TotChgAvg != 0 then NetChgAvg / TotChgAvg else 0;

def RSI = 50 * (ChgRatio + 1);

def condition2 = RSI >= 50;

#MFI

input MFI_Length = 14;

def MFIover_Sold = 20;

def MFIover_Bought = 80;

def movingAvgLength = 1;

def MoneyFlowIndex = Average(moneyflow(high, close, low, volume, MFI_Length), movingAvgLength);

def MFIOverBought = MFIover_Bought;

def MFIOverSold = MFIover_Sold;

def condition3 = MoneyFlowIndex > 50;

#Intermediate Forecast

def na = Double.NaN;

def MidLine = 50;

def Momentum = MarketForecast().Momentum;

def NearT = MarketForecast().NearTerm;

def Intermed = MarketForecast().Intermediate;

def OB = 80;

def OS = 20;

def upperLine = 110;

def condition4 = Intermed[3] <= Intermed;

#Nearterm Forecast

def condition5 = NearT >= MidLine;

#VWAP_Pivot Signals

def n = 20;

def ticks = 2.0;

def bnOK = barNumber() > n;

def isHigher = fold i = 1 to n + 1 with p = 1 while p do high > GetValue(high, -i);

def HH = if bnOK and isHigher and high == Highest(high, n)then high else Double.NaN;

def isLower = fold j = 1 to n + 1 with q = 1 while q do low < GetValue(low, -j);

def LL = if bnOK and isLower and low == Lowest(low, n) then low else Double.NaN;

def PivH = if HH > 0 then HH else Double.NaN;

def PivL = if LL > 0 then LL else Double.NaN;

plot UpPivotLow = !isNaN(PivL);

UpPivotLow.SetPaintingStrategy(PaintingStrategy.BOOLEAN_ARROW_UP);

UpPivotLow.SetLineWeight(3);

UpPivotLow.SetDefaultColor(Color.GREEN);

plot DownPivotHigh = !isNaN(PivH);

DownPivotHigh.SetPaintingStrategy(PaintingStrategy.BOOLEAN_ARROW_DOWN);

DownPivotHigh.SetLineWeight(3);

DownPivotHigh.SetDefaultColor(Color.RED);

def condition6 = !isNaN(PivL);

#EMA_1

input EMA_length = 20;

def displace = 0;

def AvgExp = ExpAverage(price[-displace], EMA_length);

def condition7 = price >= AvgExp;

#EMA_2

input EMA_2length = 50;

def displace2 = 0;

def AvgExp2 = ExpAverage(price[-displace2], EMA_2length);

def condition8 = price >= AvgExp2;

#DMI Oscillator

input DMI_length = 10;

input DMI_averageType = AverageType.WILDERS;

def diPlus = DMI(DMI_length, DMI_averageType)."DI+";

def diMinus = DMI(DMI_length, DMI_averageType)."DI-";

def Osc = diPlus - diMinus;

def Hist = Osc;

def ZeroLine = 0;

def condition9 = Osc > ZeroLine;

#Trend_Periods

input TP_fastLength = 7;

input TP_slowLength = 15;

def Periods = sign(ExpAverage(close, TP_fastLength) - ExpAverage(close, TP_slowLength));

def condition10 = Periods > 0;

#Polarized Fractal Efficiency

input PFE_length = 10;

input smoothingLength = 5;

def PFE_diff = close - close[PFE_length - 1];

def val = 100 * Sqrt(Sqr(PFE_diff) + Sqr(PFE_length)) / sum(Sqrt(1 + Sqr(close - close[1])), PFE_length - 1);

def PFE = ExpAverage(if PFE_diff > 0 then val else -val, smoothingLength);

def UpperLevel = 50;

def LowerLevel = -50;

def condition11 = PFE > ZERoLine;

#Bollinger Bands PercentB

input BBPB_averageType = AverageType.Simple;

input BBPB_length = 20;

def Num_Dev_Dn = -2.0;

def Num_Dev_up = 2.0;

def upperBand = BollingerBands(price, displace, BBPB_length, Num_Dev_Dn, Num_Dev_up, BBPB_averageType).UpperBand;

def lowerBand = BollingerBands(price, displace, BBPB_length, Num_Dev_Dn, Num_Dev_up, BBPB_averageType).LowerBand;

def PercentB = (price - lowerBand) / (upperBand - lowerBand) * 100;

def HalfLine = 50;

def UnitLine = 100;

def condition12 = PercentB > 50;

#Chaikin Oscillator

input ChaikinOsc_longLength = 10;

input ChaikinOsc_shortLength = 3;

def accDist = AccDist();

def COSC = ExpAverage(accDist, ChaikinOsc_shortLength) - ExpAverage(accDist, ChaikinOsc_longLength);

def condition13 = COSC > zeroline;

#Trend Confirmation

#Confirmation_Factor range 1-13.

input Confirmation_Factor = 6;

#Use for testing conditions individually. Remove # from line below and chang Confirmation_Factor to 1.

#def Agreement_Level = condition1;

def Agreement_Level = condition1 + condition2 + condition3 + condition4 + condition5 + condition6 + condition7 + condition8 + condition9 + condition10 + condition11 + condition12 + condition13;

input coloredCandlesOn = yes;

def UP = Agreement_Level >= Confirmation_Factor;

def DOWN = Agreement_Level < Confirmation_Factor;

AssignPriceColor(if coloredCandlesOn and UP then Color.LIGHT_GREEN else if coloredCandlesOn and DOWN then Color.RED else Color.YELLOW);

#Additional Signals

plot UPSignal = Agreement_Level crosses above Confirmation_Factor;

UPSignal.SetPaintingStrategy(PaintingStrategy.BOOLEAN_ARROW_UP);

UPSignal.SetLineWeight(1);

UPSignal.SetDefaultColor(Color.green);

plot DOWNSignal = Agreement_Level crosses below Confirmation_Factor;

DOWNSignal.SetPaintingStrategy(PaintingStrategy.BOOLEAN_ARROW_DOWN);

DOWNSignal.SetLineWeight(1);

DOWNSIGNAL.SetDefaultColor(Color.red);

I found one of your previous confirmation candle scripts here:

Looks interesting on overbought and oversold zones on a 5 minute and 1 minute chart.

Are you still using this. What do the large and smaller arrows represent and also wanted to know if it repaints?

#Confirmation Candles developed 04/15/2021 by Christopher Wilson

#Select the level of agreement among the 13 indicators included.

#MACD with Price

declare upper;

def price = close;

def fastLength = 12;

def slowLength = 26;

def MACDLength = 9;

input MACD_AverageType = {SMA, default EMA};

def MACDLevel = 0.0;

def fastEMA = ExpAverage(price, fastLength);

def slowEMA = ExpAverage(price, slowLength);

def Value;

def Avg;

switch (MACD_AverageType) {

case SMA:

Value = Average(price, fastLength) - Average(price, slowLength);

Avg = Average(Value, MACDLength);

case EMA:

Value = fastEMA - slowEMA;

Avg = ExpAverage(Value, MACDLength);}

def Diff = Value - Avg;

def Level = MACDLevel;

def condition1 = Value >= MACDLevel;

#RSI

input RSI_length = 14;

input RSI_AverageType = AverageType.WILDERS;

def NetChgAvg = MovingAverage(RSI_AverageType, price - price[1], RSI_length);

def TotChgAvg = MovingAverage(RSI_AverageType, AbsValue(price - price[1]), RSI_length);

def ChgRatio = if TotChgAvg != 0 then NetChgAvg / TotChgAvg else 0;

def RSI = 50 * (ChgRatio + 1);

def condition2 = RSI >= 50;

#MFI

input MFI_Length = 14;

def MFIover_Sold = 20;

def MFIover_Bought = 80;

def movingAvgLength = 1;

def MoneyFlowIndex = Average(moneyflow(high, close, low, volume, MFI_Length), movingAvgLength);

def MFIOverBought = MFIover_Bought;

def MFIOverSold = MFIover_Sold;

def condition3 = MoneyFlowIndex > 50;

#Intermediate Forecast

def na = Double.NaN;

def MidLine = 50;

def Momentum = MarketForecast().Momentum;

def NearT = MarketForecast().NearTerm;

def Intermed = MarketForecast().Intermediate;

def OB = 80;

def OS = 20;

def upperLine = 110;

def condition4 = Intermed[3] <= Intermed;

#Nearterm Forecast

def condition5 = NearT >= MidLine;

#VWAP_Pivot Signals

def n = 20;

def ticks = 2.0;

def bnOK = barNumber() > n;

def isHigher = fold i = 1 to n + 1 with p = 1 while p do high > GetValue(high, -i);

def HH = if bnOK and isHigher and high == Highest(high, n)then high else Double.NaN;

def isLower = fold j = 1 to n + 1 with q = 1 while q do low < GetValue(low, -j);

def LL = if bnOK and isLower and low == Lowest(low, n) then low else Double.NaN;

def PivH = if HH > 0 then HH else Double.NaN;

def PivL = if LL > 0 then LL else Double.NaN;

plot UpPivotLow = !isNaN(PivL);

UpPivotLow.SetPaintingStrategy(PaintingStrategy.BOOLEAN_ARROW_UP);

UpPivotLow.SetLineWeight(3);

UpPivotLow.SetDefaultColor(Color.GREEN);

plot DownPivotHigh = !isNaN(PivH);

DownPivotHigh.SetPaintingStrategy(PaintingStrategy.BOOLEAN_ARROW_DOWN);

DownPivotHigh.SetLineWeight(3);

DownPivotHigh.SetDefaultColor(Color.RED);

def condition6 = !isNaN(PivL);

#EMA_1

input EMA_length = 20;

def displace = 0;

def AvgExp = ExpAverage(price[-displace], EMA_length);

def condition7 = price >= AvgExp;

#EMA_2

input EMA_2length = 50;

def displace2 = 0;

def AvgExp2 = ExpAverage(price[-displace2], EMA_2length);

def condition8 = price >= AvgExp2;

#DMI Oscillator

input DMI_length = 10;

input DMI_averageType = AverageType.WILDERS;

def diPlus = DMI(DMI_length, DMI_averageType)."DI+";

def diMinus = DMI(DMI_length, DMI_averageType)."DI-";

def Osc = diPlus - diMinus;

def Hist = Osc;

def ZeroLine = 0;

def condition9 = Osc > ZeroLine;

#Trend_Periods

input TP_fastLength = 7;

input TP_slowLength = 15;

def Periods = sign(ExpAverage(close, TP_fastLength) - ExpAverage(close, TP_slowLength));

def condition10 = Periods > 0;

#Polarized Fractal Efficiency

input PFE_length = 10;

input smoothingLength = 5;

def PFE_diff = close - close[PFE_length - 1];

def val = 100 * Sqrt(Sqr(PFE_diff) + Sqr(PFE_length)) / sum(Sqrt(1 + Sqr(close - close[1])), PFE_length - 1);

def PFE = ExpAverage(if PFE_diff > 0 then val else -val, smoothingLength);

def UpperLevel = 50;

def LowerLevel = -50;

def condition11 = PFE > ZERoLine;

#Bollinger Bands PercentB

input BBPB_averageType = AverageType.Simple;

input BBPB_length = 20;

def Num_Dev_Dn = -2.0;

def Num_Dev_up = 2.0;

def upperBand = BollingerBands(price, displace, BBPB_length, Num_Dev_Dn, Num_Dev_up, BBPB_averageType).UpperBand;

def lowerBand = BollingerBands(price, displace, BBPB_length, Num_Dev_Dn, Num_Dev_up, BBPB_averageType).LowerBand;

def PercentB = (price - lowerBand) / (upperBand - lowerBand) * 100;

def HalfLine = 50;

def UnitLine = 100;

def condition12 = PercentB > 50;

#Chaikin Oscillator

input ChaikinOsc_longLength = 10;

input ChaikinOsc_shortLength = 3;

def accDist = AccDist();

def COSC = ExpAverage(accDist, ChaikinOsc_shortLength) - ExpAverage(accDist, ChaikinOsc_longLength);

def condition13 = COSC > zeroline;

#Trend Confirmation

#Confirmation_Factor range 1-13.

input Confirmation_Factor = 6;

#Use for testing conditions individually. Remove # from line below and chang Confirmation_Factor to 1.

#def Agreement_Level = condition1;

def Agreement_Level = condition1 + condition2 + condition3 + condition4 + condition5 + condition6 + condition7 + condition8 + condition9 + condition10 + condition11 + condition12 + condition13;

input coloredCandlesOn = yes;

def UP = Agreement_Level >= Confirmation_Factor;

def DOWN = Agreement_Level < Confirmation_Factor;

AssignPriceColor(if coloredCandlesOn and UP then Color.LIGHT_GREEN else if coloredCandlesOn and DOWN then Color.RED else Color.YELLOW);

#Additional Signals

plot UPSignal = Agreement_Level crosses above Confirmation_Factor;

UPSignal.SetPaintingStrategy(PaintingStrategy.BOOLEAN_ARROW_UP);

UPSignal.SetLineWeight(1);

UPSignal.SetDefaultColor(Color.green);

plot DOWNSignal = Agreement_Level crosses below Confirmation_Factor;

DOWNSignal.SetPaintingStrategy(PaintingStrategy.BOOLEAN_ARROW_DOWN);

DOWNSignal.SetLineWeight(1);

DOWNSIGNAL.SetDefaultColor(Color.red);