#Trade ideas from Verniman

#Original Logic from STB Usethinkscript 7/20

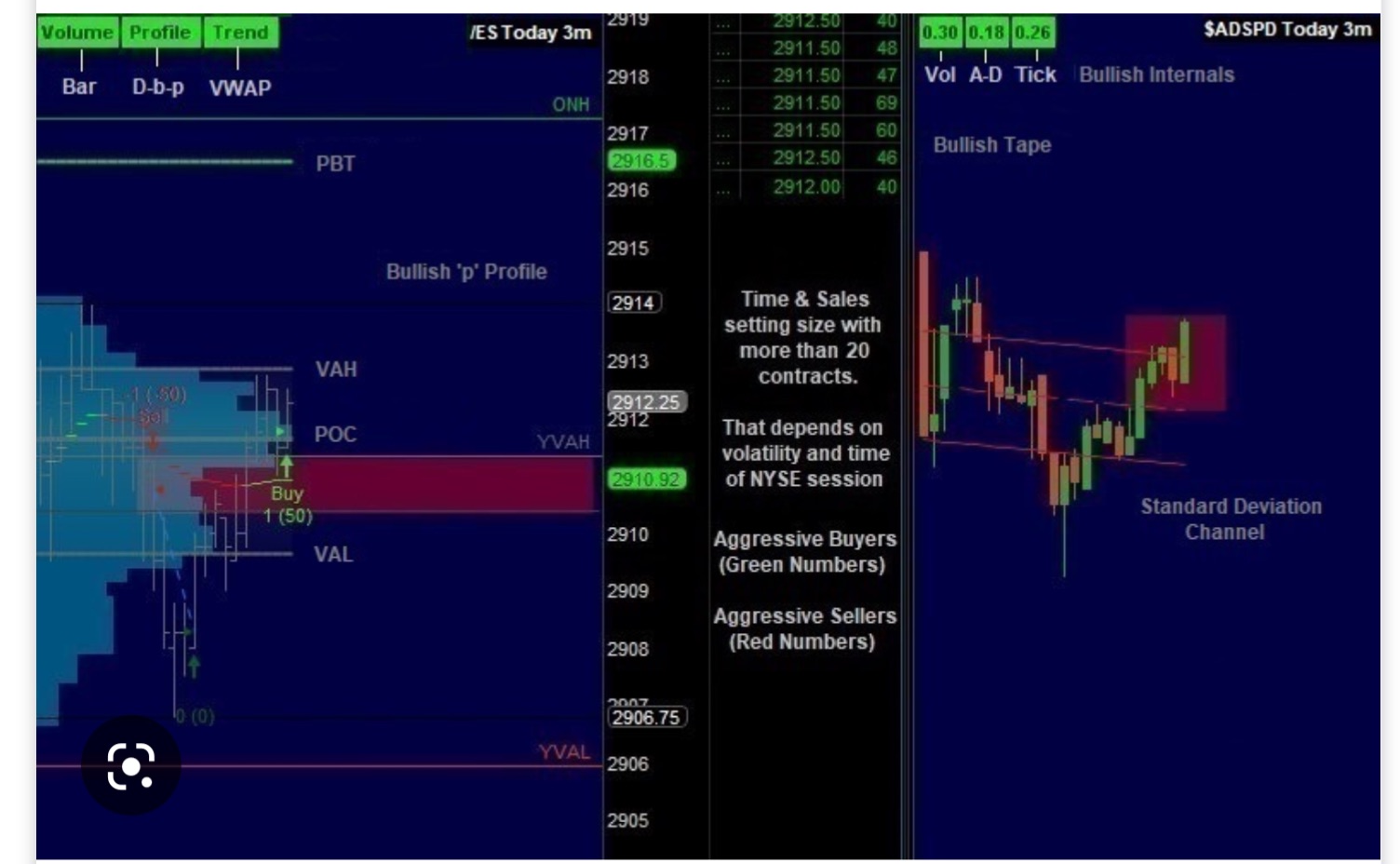

#Trade above below vwap

#Past posts (now deleted) indicated BSP, Demand Index, STO, Volume, SPX Cash Internals, and levels

#Most trades are breakout based above below VWAP

#RSI has given the best mirror for trades from 2020-22

###### TIME ######

input zoneStartAM = 930;

input zoneEndAM = 1200;

input zoneStartPM = 1330;

input zoneEndPM = 1600;

input zoneEndclose = 1609;

input type = {default NOTRADE, REVERSAL};

input price = close;

input length = 5;

input over_bought = 70;

input over_sold = 30;

input rsiAverageType = AverageType.SIMPLE;

input MALength = 2;

def rsi = reference RSI(price = price, length = length, averageType = rsiAverageType);

def RSIMA = Average(rsi, MALength);

#AddOrder(OrderType.BUY_AUTO, rsi crosses above over_sold, tickColor = GetColor(0), arrowColor = #GetColor(0), name = "RSI_LE");

#AddOrder(OrderType.SELL_AUTO, rsi crosses below over_bought, tickColor = GetColor(1), arrowColor = #GetColor(1), name = "RSI_SE");

def highBar;

def lowBar;

def highBar2;

def lowBar2;

switch (type){

case NOTRADE:

highBar = if SecondsTillTime(zoneStartAM) <= 0 and SecondsTillTime(zoneEndAM) >= 0 then HighestAll(open) else Double.NaN;

lowBar = if SecondsTillTime(zoneStartAM) <= 0 and SecondsTillTime(zoneEndAM) >= 0 then LowestAll(close) else Double.NaN;

case REVERSAL:

lowBar = if SecondsTillTime(zoneStartAM) <= 0 and SecondsTillTime(zoneEndAM) >= 0 then HighestAll(open) else Double.NaN;

highBar = if SecondsTillTime(zoneStartAM) <= 0 and SecondsTillTime(zoneEndAM) >= 0 then LowestAll(close) else Double.NaN;

}

switch (type){

case NOTRADE:

highBar2 = if SecondsTillTime(zoneStartPM) <= 0 and SecondsTillTime(zoneEndPM) >= 0 then HighestAll(open) else Double.NaN;

lowBar2 = if SecondsTillTime(zoneStartPM) <= 0 and SecondsTillTime(zoneEndPM) >= 0 then LowestAll(close) else Double.NaN;

case REVERSAL:

lowBar2 = if SecondsTillTime(zoneStartPM) <= 0 and SecondsTillTime(zoneEndPM) >= 0 then HighestAll(open) else Double.NaN;

highBar2 = if SecondsTillTime(zoneStartPM) <= 0 and SecondsTillTime(zoneEndPM) >= 0 then LowestAll(close) else Double.NaN;

}

###### TIME END #####

def adspdl = low("$adspd");

def adspdh = high("$adspd");

def adspdc = close("$adspd");

def volspd = close("$volspd");

def HMA = MovingAverage(AverageType.HULL, close, 21);

input numDevDn = -2.0;

input numDevUp = 2.0;

input timeFrame = {default DAY, WEEK, MONTH};

def cap = GetAggregationPeriod();

def errorInAggregation =

timeFrame == timeFrame.DAY and cap >= AggregationPeriod.WEEK or

timeFrame == timeFrame.WEEK and cap >= AggregationPeriod.MONTH;

Assert(!errorInAggregation, "timeFrame should be not less than current chart aggregation period");

def yyyyMmDd = GetYYYYMMDD();

def periodIndx;

switch (timeFrame) {

case DAY:

periodIndx = yyyyMmDd;

case WEEK:

periodIndx = Floor((DaysFromDate(First(yyyyMmDd)) + GetDayOfWeek(First(yyyyMmDd))) / 7);

case MONTH:

periodIndx = RoundDown(yyyyMmDd / 100, 0);

}

def isPeriodRolled = CompoundValue(1, periodIndx != periodIndx[1], yes);

def volumeSum;

def volumeVwapSum;

def volumeVwap2Sum;

if (isPeriodRolled) {

volumeSum = volume;

volumeVwapSum = volume * vwap;

volumeVwap2Sum = volume * Sqr(vwap);

} else {

volumeSum = CompoundValue(1, volumeSum[1] + volume, volume);

volumeVwapSum = CompoundValue(1, volumeVwapSum[1] + volume * vwap, volume * vwap);

volumeVwap2Sum = CompoundValue(1, volumeVwap2Sum[1] + volume * Sqr(vwap), volume * Sqr(vwap));

}

def price1 = volumeVwapSum / volumeSum;

def deviation = Sqrt(Max(volumeVwap2Sum / volumeSum - Sqr(price1), 0));

def VWAP = price1;

#AssignPriceColor(if adspdl < adspdl[1] && close < vwap && close< hma && volume > volume[1] then #Color.RED else if adspdh > adspdh[1] && close > vwap && close > hma && volume>volume[1] then #Color.GREEN else Color.GRAY);

####LONGS####

AddOrder(OrderType.BUY_TO_OPEN, SecondsTillTime(zoneStartAM) <= 0 && SecondsTillTime(zoneEndAM) >= 0 and open > VWAP && VWAP > VWAP[1] && RSIMA crosses above over_bought, name = "Buy open AM @" + open[-1], 1, Color.ORANGE, Color.GREEN);

AddOrder(OrderType.BUY_TO_OPEN,secondsTillTime(zoneStartpM) <= 0 && secondsTillTime(zoneEndpM) >= 0 and open > vwap && vwap>vwap[1] && RSIMA crosses above over_bought, name = "Buy open AM @"+open[-1], 1, Color.ORANGE, Color.green);

##SHORTS###

#Changed close to open>vwap

AddOrder(OrderType.SELL_TO_OPEN, SecondsTillTime(zoneStartAM) <= 0 && SecondsTillTime(zoneEndAM) >= 0 and open < VWAP && VWAP < VWAP[1] && RSIMA crosses below over_sold, name = "Sell open AM @" + open[-1], 1, Color.ORANGE, Color.RED);

AddOrder(OrderType.SELL_TO_OPEN, SecondsTillTime(zoneStartPM) <= 0 && SecondsTillTime(zoneEndPM) >= 0 and open < VWAP && VWAP < VWAP[1] && RSIMA crosses below over_sold, name = "Sell open PM @" + open[-1], 1, Color.ORANGE, Color.RED);

####Close orders######

AddOrder(OrderType.SELL_TO_CLOSE, RSIMA crosses below over_bought, name = "Sell close @" + open[-1], 1, Color.ORANGE, Color.RED);

AddOrder(OrderType.BUY_TO_CLOSE, RSIMA crosses above over_sold, name = "Buy close @" + open[-1], 1, Color.ORANGE, Color.RED);

###Market close orders####

AddOrder(OrderType.BUY_TO_CLOSE, SecondsTillTime(zoneEndclose) <= 0, name = "Buy Market Close @" + open[-1], 1, Color.ORANGE, Color.RED);

AddOrder(OrderType.SELL_TO_CLOSE, SecondsTillTime(zoneEndclose) <= 0, name = "Sell Market Close @" + open[-1], 1, Color.ORANGE, Color.RED);