Author Message:

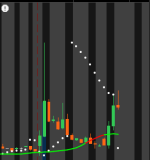

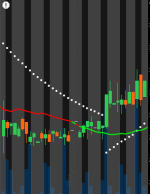

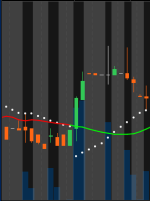

The Kalman PSaR combines the well-known Parabolic SAR (PSaR) with the advanced smoothing capabilities of the Kalman Filter. This innovative tool aims to enhance the traditional PSaR by integrating Kalman filtering, which reduces noise and improves trend detection. The Kalman PSaR adapts dynamically to price movements, making it a highly effective indicator for spotting trend shifts while minimizing the impact of false signals caused by market volatility.

CODE:

CSS:

# // Indicator for TOS

#// © BackQuant

# indicator(title="Kalman PSaR [BackQuant]", shorttitle = "KPSaR [BackQuant]"

# Converted by Sam4Cok@Samer800 - 09/2024

input timeframe = AggregationPeriod.MIN;

input ProcessNoise = 0.03; # "Process Noise"

input MeasurementNoise = 3.0; # "Measurement Noise"

input MinStep = 0.02; # "Min Step"

input MaxStep = 0.1; # "Max Step"

input Acceleration = 0.02; # "Acceleration"

input smoothing = yes; # "Use Smoothing?"

input smoothingMaType = {Default "SMA", "HULL", "EMA", "WMA", "DEMA", "RMA", "LINREG", "TEMA"};# "Smoothing MA"

input SmoothingPeriod = 10; # "Smoothing Period"

input colorBars = no; # "Paint candles according to Trend?"

input showPsar = yes; # "Show PSaR on Chart?"

def na = Double.NaN;

def current = GetAggregationPeriod();

def tf = Max(current, timeframe);

#-- TV PSAR

script sar {

input start = 0.02;

input inc = 0.02;

input max = 0.2;

input h = high;

input l = low;

input hi = high;

input lo = low;

input cl = close;

def na = Double.NaN;

def bar = bar[1] + 1;

def startTrend = cl > cl[1];

def maxMin;

def result;

def acceleration ;

def isBelow;

def isFirstTrendBar;

def sar;

def maxMin2;

def acceleration2;

def isBelow1;

def isFirstTrendBar1;

def acceleration1;

def maxMin1;

def result11;

if bar == 1 {

isFirstTrendBar1 = yes;

acceleration1 = start;

if startTrend {

isBelow1 = yes;

maxMin1 = h;

result11 = l[1];

} else {

isBelow1 = no;

maxMin1 = l;

result11 = h[1];

}

} else {

isBelow1 = isBelow[1];

maxMin1 = CompoundValue(1, maxMin2[1], if startTrend then h else l);

result11 = CompoundValue(1, sar[1], if startTrend then l[1] else h[1]);

isFirstTrendBar1 = no;

acceleration1 = acceleration2[1];

}

def result1 = CompoundValue(1, result11 + acceleration1 * (maxMin1 - result11), result11);

if isBelow[1] {

if result[1] > lo {

isFirstTrendBar = yes;

isBelow = no;

result = max(h, maxMin1);

maxMin = l;

acceleration = start;

} else {

maxMin = maxMin1;

acceleration = acceleration1;

isFirstTrendBar = isFirstTrendBar1;

isBelow = isBelow1;

result = result1;

}

} else {

if result[1] < hi {

isFirstTrendBar = yes;

isBelow = yes;

result = min(l , maxMin1);

maxMin = h;

acceleration = start;

} else {

acceleration = acceleration1;

maxMin = maxMin1;

isFirstTrendBar = isFirstTrendBar1;

isBelow = isBelow1;

result = result1;

}}

if !isFirstTrendBar {

if isBelow {

if hi > maxMin {

maxMin2 = h;

acceleration2 = min(acceleration + inc, max);

} else {

maxMin2 = maxMin;

acceleration2 = acceleration;

}

} else {

if l < maxMin {

maxMin2 = l;

acceleration2 = min(acceleration + inc, max);

} else {

maxMin2 = maxMin;

acceleration2 = acceleration;

}}

} else {

maxMin2 = maxMin;

acceleration2 = acceleration;

}

sar = if isBelow then if bar > 1 then Min(result, l[2]) else Min(result, l[1]) else

if bar > 1 then max(result, h[2]) else max(result, h[1]);

plot psar = if !isNaN(close) then sar else Double.NaN;

}

script f_kalman {

input src = close;

input processNoise_kRoc = 0.03;

input measurementNoise_kRoc = 3.0;

def errorCovariance;

def stateEstimate;

def errorCovariance1 = CompoundValue(1, if !errorCovariance[1] then 1 else errorCovariance[1], 100);

def stateEstimate1 = CompoundValue(1, if !stateEstimate[1] then src else stateEstimate[1], src);

def predictedErrorCovariance = errorCovariance1 + processNoise_kRoc;

def kg = predictedErrorCovariance / (predictedErrorCovariance + measurementNoise_kRoc);

stateEstimate = stateEstimate1 + kg * (src - stateEstimate1);

errorCovariance = (1 - kg) * predictedErrorCovariance;

plot out = stateEstimate;

}

def kalman_close = f_kalman(close(Period = tf), ProcessNoise, MeasurementNoise);

def kalman_high = f_kalman(high(Period = tf) , ProcessNoise, MeasurementNoise);

def kalman_low = f_kalman(low(Period = tf) , ProcessNoise, MeasurementNoise);

def psarKal = sar(MinStep, Acceleration, MaxStep, kalman_high, kalman_low,

high(Period = tf), low(Period = tf), close(Period = tf) );

def psar;

if smoothing {

Switch (smoothingMaType) {

Case "HULL" : psar = HullMovingAvg(psarKal, SmoothingPeriod);

Case "EMA" : psar = ExpAverage(psarKal, SmoothingPeriod);

Case "WMA" : psar = WMA(psarKal, SmoothingPeriod);

Case "DEMA" : psar = DEMA(psarKal, SmoothingPeriod);

Case "RMA" : psar = WildersAverage(psarKal, SmoothingPeriod);

Case "LINREG" : psar = Inertia(psarKal, SmoothingPeriod);

Case "TEMA" : psar = TEMA(psarKal, SmoothingPeriod);

Default : psar = Average(psarKal, SmoothingPeriod);}

} else {

psar = psarKal;

}

def psar_long = close > psar;

def psar_short = close < psar;

def Trend = if psar_long then 1 else

if psar_short then -1 else Trend[1];

#// Plotting

plot kalmanPSAR = if showPsar then psar else na; # "Kalman PSaR"

kalmanPSAR.SetLineWeight(2);

kalmanPSAR.AssignValueColor(if Trend>0 then Color.GREEN else

if Trend<0 then Color.RED else Color.GRAY);

#-- bar color

AssignPriceColor(if !colorBars then Color.CURRENT else

if Trend>0 then Color.GREEN else

if Trend<0 then Color.RED else Color.GRAY);

#-- END of CODE